The Read · 90 secondsThe Read

Two weeks ago the market stopped paying for promises. A record Broadcom quarter got sold because the company wouldn't raise its forecast, the chip index had its worst day in over a year, and inflation came in at a three-year high. Then on Thursday, into that exact weather, SpaceX went public at the largest listing ever attempted and closed its first day near $161, well above the $135 it priced at. The exit window everyone said was shut turned out to be open.

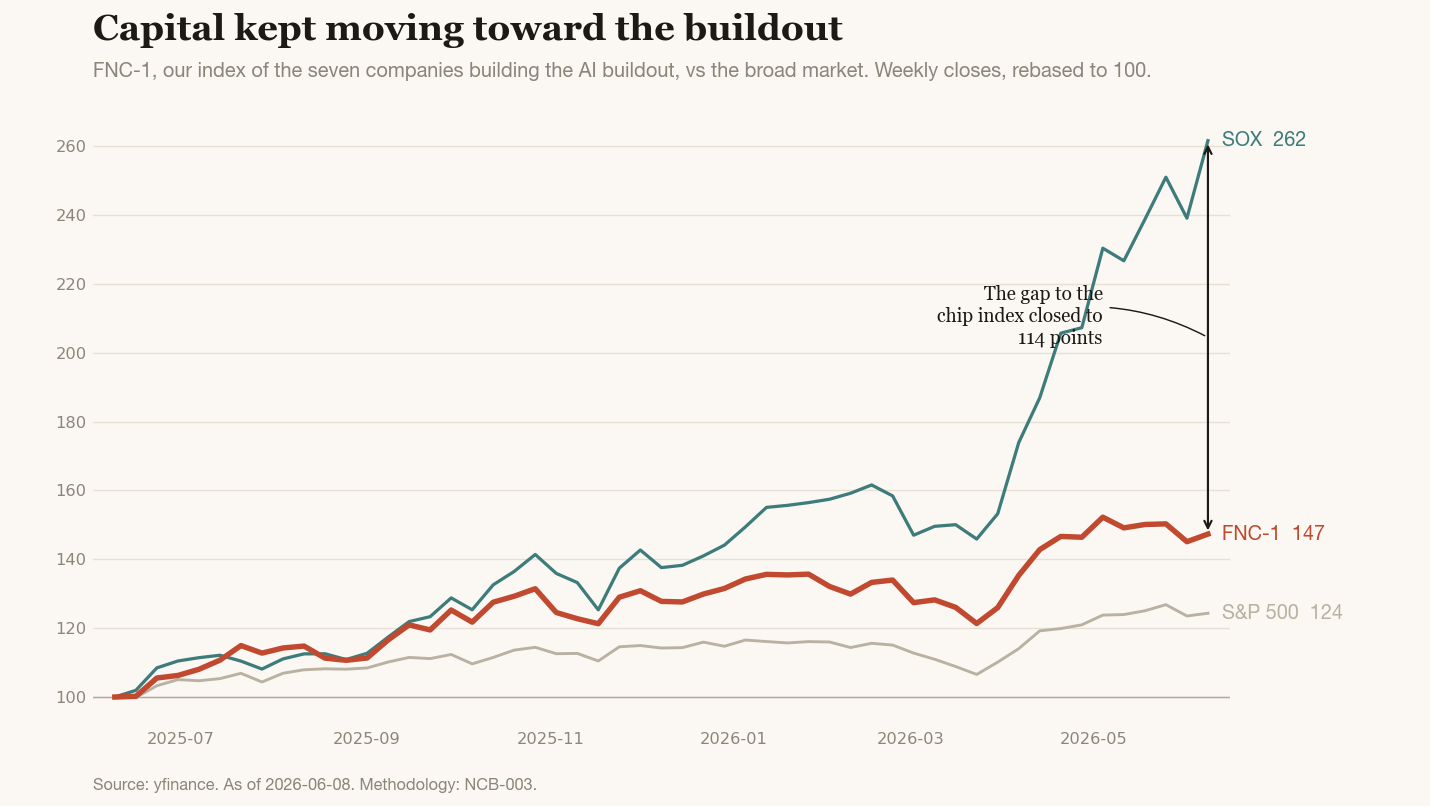

So here's the week in one line: the chips came roaring back, and the companies actually building the AI buildout did not come with them. The chip index jumped 19 points. Our basket of builders moved less than 3. That gap is the story, and it says the rebound was a chip-stock rebound, not a buildout one. Underneath, quieter but real, the betting markets cooled hard on an OpenAI IPO this year. The instruments show both moves.

FNC-1, our index of the seven companies building the AI buildout (NCB-003), reads against the SOX, the chip index most people watch, and the S&P 500. Beside it sits the Belief Index, a read on how convinced the betting markets are that the boom keeps going. When the two pull apart, the divergence is usually the most useful thing on the page.

The decision this Reading informs belongs to an allocator weighing whether to chase the semiconductor rebound. The chips ran 19 points in a week. Is that the buildout reaccelerating, or a narrower trade in names that build very little? The gap is the answer.

Capital

Money kept sitting with the companies building the buildout, but it stopped outrunning the broad market, and it fell far behind the chips. The direction matters more than the level this week: the builders held while the chips sprinted, and holding while everything around you sprints is itself a signal.

The binding events sat just outside the data window. SpaceX priced at $135 on June 12 and closed near $161 on debut, the largest listing on record at a valuation near $1.75 trillion, per Reuters. Broadcom posted a record quarter on June 3 and fell about 12% anyway, because CEO Hock Tan left the full-year target unchanged. Two sessions later the SOX fell 5.2%, its worst day since April 2025, and May CPI printed at a three-year high.

The instrument confirms the shape. FNC-1 closed the week at 147.3, up 47.3% over twelve months and barely changed from last week's 144.5. The SOX reads 261.6, up from 242.6, a sharp one-week rebound. The S&P 500 sits at 124.3. All three rebased to 100 at the start of the trailing twelve months. The numbers corroborate what the tape suggested: the chip index did the recovering, and the builder basket mostly watched.

The mechanism worth naming is what the SOX holds that FNC-1 leaves out: merchant and memory names, the parts of the chip complex most exposed to a sentiment swing. FNC-1 holds the seven companies whose capital expenditure actually builds data centers, power, and frontier models. When the chips bounce and the builders don't, the bounce lived in the names that trade on mood, not the ones that pour concrete.

NVIDIA sits at the seam. It belongs to both indices, but its recovery pulled the SOX up faster than FNC-1, because the rest of the chip index rebounded around it while the rest of the buildout basket did not.

The spread is the number to hold. The gap to the SOX widened to 114 points, from roughly 98 last week, and it widened because the chips ran, not because the builders fell. A gap that opens on the chips climbing reads as concentration in the sentiment-sensitive part of the complex. That is a different signal than a selloff, and a more revealing one.

Belief

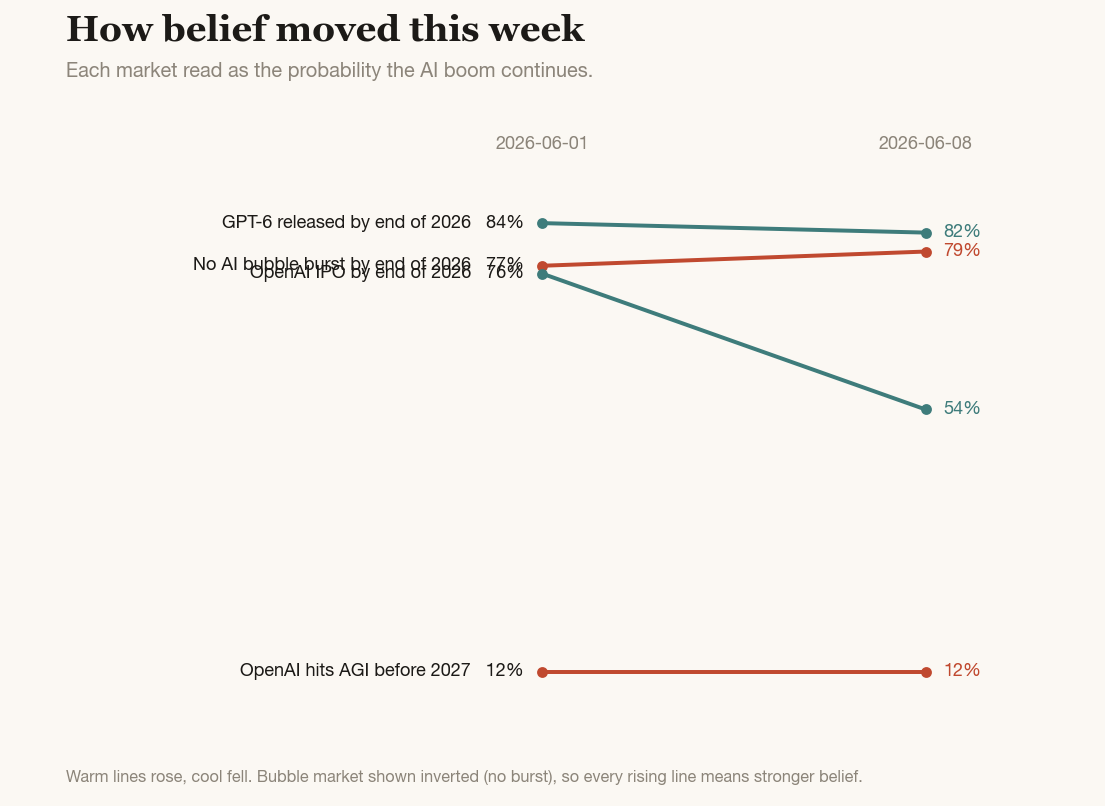

The Belief Index reads 55 this week, down from 59 at last week's reading. The first genuine cooling after a month of steady climb.

Read

Last week's capital data did one clean thing: it confirmed that the builders hold. The basket sat at 144.5 then and 147.3 now, through a fortnight that included the worst chip session since early 2025 and a three-year inflation high. The buildout's share prices did not break. The companies pouring the concrete held their ground while the market repriced the patience that funds them.

What the instrument shows that a single chip ticker cannot is the composition of this week's rebound. The SOX jumped 19 points and FNC-1 moved 3. If you watched only the chip index, you would read this week as the buildout reaccelerating. The basket says otherwise: the recovery concentrated in the merchant and memory names FNC-1 excludes, not in the names that build. The chips rebounded; the buildout did not, and only an instrument that separates them could tell you which.

Belief moved the opposite way from capital, and that is the week's real tension. The Belief Index fell four points, and almost all of it came from one market: the odds of an OpenAI IPO this year dropped from 76% to 54%. The strange part is the timing. SpaceX just proved a megacap can go public into a bad tape and pop 19%, which should, if anything, raise the odds for other big listings. Instead the market cut OpenAI's IPO odds by a fifth. The crowd is separating "the exit window is open" from "OpenAI specifically walks through it this year," and that distinction is new this week.

Put the two signals together. Capital is steady and belief is softening, and the softening is specific, not broad: the bubble-burst odds did not rise, the model-release odds barely moved, only the single most company-specific bet in the panel fell. Capital is holding the buildout while belief trims its most speculative leg. That is not the shape of a market losing faith in the buildout. It is the shape of a market that still believes in the construction and has started to doubt one of its loudest IPO stories. For the next two to six weeks, the gap to watch is whether the builders keep holding while the chips run, because a buildout basket that stays flat through a chip rally is telling you the rally has a narrow base.

What this measures, what it does not

The Belief Index is one venue's positioning, the Polymarket panel, weighted by FP1's view of which markets matter. Individual components will be wrong, and the OpenAI IPO market may reprice again next week on a single headline. The index is a directional read on conviction, not a forecast.

FNC-1 is a measurement instrument, not an investment vehicle. It is rebased weekly to track relative movement, so the basket level is less informative than the spread to the SOX. Do not read it as a portfolio.

Both fail openly. Every number here traces to the chart pipeline or a named source, every call carries a falsifier and a date, and when a read breaks we log it. The method is in NCB-003.

Cadence

The Reading runs every Monday. The next State of the Transition Briefing returns Thursday, June 25, with the full correspondent desks and the Radar delta. The standing calls, including the SpaceX exit-window read that resolves June 26, are tracked at fp1.ai/radar.

Methodology: NCB-003: FNC-1, the Novacene Composite.

Sources. Capital data via yfinance, weekly closes through June 8, 2026. Belief panel via Polymarket Gamma API. SpaceX IPO price and debit close per Reuters and first-day market coverage, June 12, 2026. Broadcom fiscal Q2 results per company release, June 3, 2026. SOX June 5 session and May CPI per Trading Economics and Bloomberg.