This week the Financial Times reported Anthropic is in advanced talks to raise up to $50 billion at a valuation approaching $1 trillion. PJM Interconnection, the largest US regional grid operator, floated curtailing electricity to new data-center loads starting summer 2026. NVDA recovered most of last week's pullback into the May 20 earnings print, and the FNC-1 to SOX spread widened to 90 points. The Belief Index ticked down on a nine-point raw move in the bubble-burst component, the largest single-component shift since the panel went live.

I. Capital

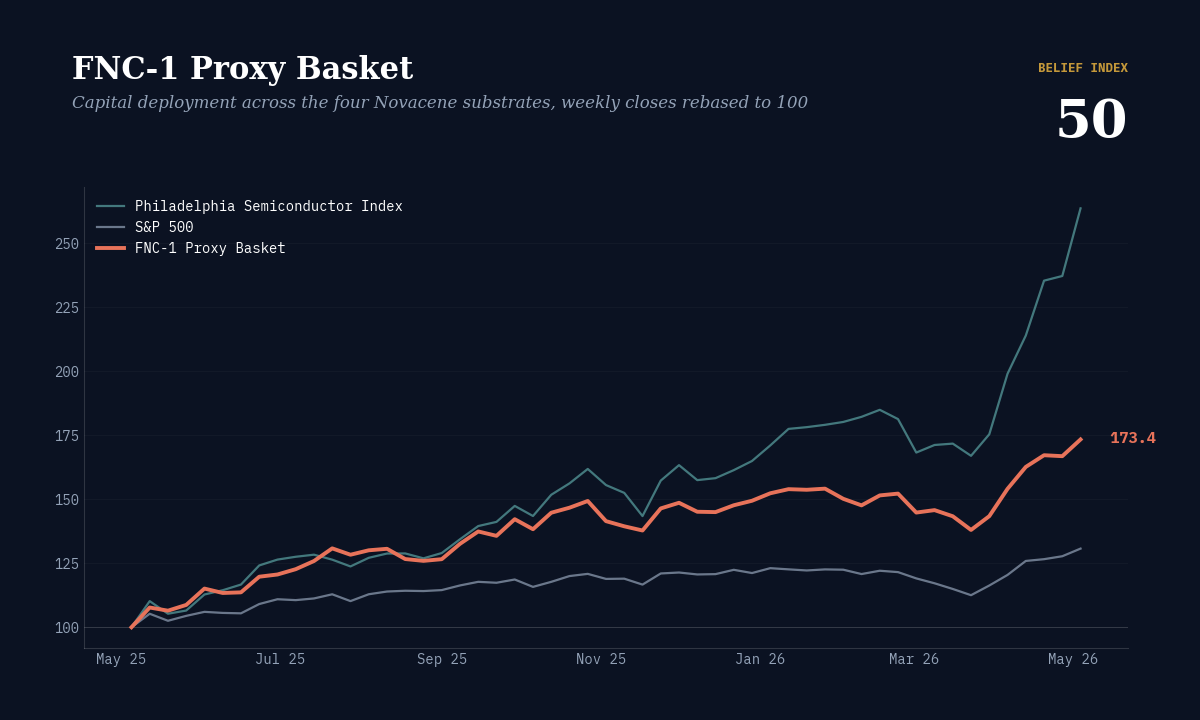

This week the FNC-1 Proxy reads 173.4, up 2.0 points from 171.4 at the May 1 close. The Philadelphia Semiconductor Index reads 263.6, up 16.3 points from 247.3. The S&P 500 reads 130.7, up 1.0 from 129.7. All three rebased to 100 at the start of the inaugural twelve-month window.

The week's binding capital event came on Friday. The Financial Times reported that Anthropic is in discussions for a funding round of up to $50 billion that could value the company at close to $1 trillion, with Dragoneer Investment Group, General Catalyst, and Lightspeed Venture Partners among the named participants. CFO Krishna Rao is leading the talks, with a close expected within two months, and Anthropic's annualized revenue is on the verge of $45 billion, a fivefold increase from $9 billion at the end of 2024. The round, if it prints at the high end, would clear OpenAI's $852 billion mark from March 2026 and reset the private-market AI ceiling roughly $500 billion above Anthropic's $380 billion close in February. The PJM Interconnection memo released the same week, titled “Powering Reliability Through Market Design,” named the transition from “an era of managing surplus to an era of managing scarcity,” and proposed that “unbacked new large load additions” be curtailed first during supply shortages while residential loads are insulated.

The headline on Anthropic is the valuation. The headline below the valuation is the revenue trajectory. A fivefold growth print in eighteen months from $9 billion to $45 billion annualized reframes what the hyperscaler capex commitments confirmed at last week's earnings cluster were paying for. The PJM memo is the structural counterpart. R-006 named HBM memory as the new constraint inside Compute. PJM names grid power as the second hard constraint, this time inside Energy. Two of the four substrates are running into physical limits simultaneously, and the limits emerged in the same week.

NVDA closed Friday at $215.20, a third consecutive up day, recovering most of the 8.4% pullback that R-006 named after the April 27 all-time high of $216.61. Consensus for the May 20 fiscal Q1 print sits near $78.8 billion revenue, with 37 analysts at a $272 consensus target and Goldman Sachs at $250. The leader firming again into earnings while the SOX kept running gives the substrate a different shape than it had seven days ago.

The FNC-1 to SOX spread widened from 75.9 points last week to 90.2 points this week. The 14-point move is the largest weekly widening in the spread since the inaugural reading. Capital is broadening within the chip complex faster than the diversified basket can absorb, which is exactly what the multi-stock construction was designed to surface.

II. Belief

The Belief Index reads 50 this week, down from 52 at the May 4 reading. Three of four components moved, and the largest-weighted component moved most.

III. Read

The capital data confirmed two things this week. The FNC-1 to SOX spread widens when capital rotates within the chip complex faster than the diversified basket can absorb, and the 14-point spread move in seven days is the cleanest example of that mechanic the panel has produced. The substrate ranking is also now defined by physical constraints rather than by capital availability. HBM is sold out through 2026. PJM is preparing to curtail new data-center loads beginning this summer. Two substrates, two constraints, in the same week.

The move worth naming is internal to the panel. The bubble-burst component moved nine points raw, the largest single-component shift since the inaugural reading. Because the component carries 30% panel weight and is inverted, it is the primary driver of the composite move from 52 to 50. The other three components moved a combined eight points in mixed directions and netted close to flat. The four-component decomposition is doing what the methodology said it would, showing which belief is repricing rather than only that the index moved. A single-number sentiment read would have shown the panel ticked down by two. The decomposition shows that two-thirds of prediction-market participants still bet against a bubble break this year, but the cohort betting on one grew by more than half in seven days.

What Issue 005 called the dominant belief, “this is not a bubble,” cracked further. The Anthropic FT print is the specific catalyst. A private company tripling its valuation in three months on a fivefold revenue print reads as either vindication of the structural capex thesis or the canonical late-cycle marker, and the Polymarket panel is now pricing both readings simultaneously. The Bank of England note circulating this week named OpenAI's ramp from $157 billion to $500 billion in twelve months as the institutional flag. The Allianz capex-cycle note this week framed the same data differently, putting the AI capex-to-revenue divergence at roughly 46% versus the 32% divergence observed during the 2001 telecom cycle. The IPO timing softens further, the structural capex thesis hardens, and conviction in the absence of a break weakens. Those are not the same shifts.

The two signals together point at something the FNC-1 to SOX spread is positioned to surface over the next four to six weeks. Capital is broadening into the chip complex while conviction in the structural story weakens at the margin. If NVDA prints in line on May 20 and the spread holds at 90 points or widens, the basket has done its work. If NVDA disappoints and the spread compresses, the bubble cohort gets its first hard data point. The Anthropic round closing inside two months, at whatever final number, will be the second.

IV. What this measures, what it does not

The Belief Index is a snapshot of one venue's positioning, weighted by FP1's view of which markets matter for the AI transition. Individual components will be wrong. The aggregate, over time, is the signal.

The FNC-1 Proxy is a measurement instrument, not an investment vehicle. When divergence between FNC-1 and the SOX widens or compresses, that is data. The Belief Index helps frame what the divergence means.

Both instruments fail openly. NCB-003 specifies the falsification triggers.

V. Cadence

The Capital and Belief panel runs every Monday. The longer-form State of the Transition Briefing returns Thursday, May 14 (B-001) with a Radar delta and the first substrate sub-index breakdown.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through May 8, 2026

- Financial Times, “Anthropic weighs deal for near $1tn valuation as revenue surges”, May 8, 2026

- Reuters wire on FT Anthropic report, May 8, 2026

- PJM Interconnection, “Powering Reliability Through Market Design”, May 6, 2026

- The Information and Wall Street Journal continued reporting on OpenAI CFO Sarah Friar and IPO timing, May 5–10, 2026

- NVIDIA Corporation closing prices via Nasdaq, May 5–8, 2026

- Bank of England Financial Policy Committee, AI valuation risk note, May 2026

- Allianz Global Investors, “AI Capex Cycle” research note, May 2026

- Polymarket — OpenAI achieves AGI before 2027

- Polymarket — GPT-6 released by Dec 31, 2026

- Polymarket — OpenAI IPO by Dec 31, 2026

- Polymarket — AI bubble burst by Dec 31, 2026

Capital broadened. Belief softened.

Two substrates hit physical limits in the same week.

The cohort that funded the cycle is being repriced.

The spread is widening. The Read follows the spread.