This week the four largest US hyperscalers reported Q1 2026 earnings on the same day. Combined 2026 capex commitments across the five largest names now sit at the high end of consensus. NVIDIA hit an all-time high on April 27 and gave back roughly 8% by Friday. The Belief Index ticked down on coordinated softening across three of four panel components.

I. Capital

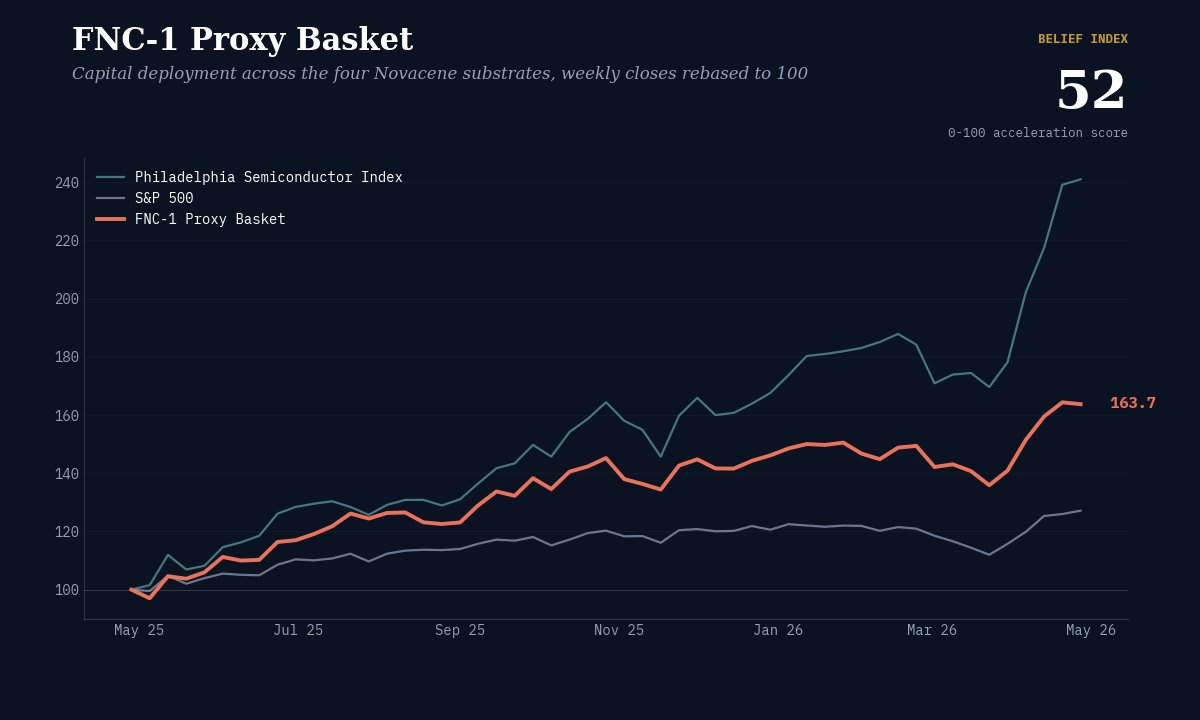

This week the FNC-1 Proxy reads 163.7 over the trailing twelve months. The Philadelphia Semiconductor Index reads 241.0. The S&P 500 reads 127.1. All three rebased to 100 at the start of the trailing window.

The Q1 earnings cluster on April 29 was the week's binding event. Microsoft guided to $190 billion in FY26 capex with Azure capacity-constrained through year-end, attributing roughly $25 billion of the increase to higher component costs. Alphabet raised its 2026 capex band to $180–190 billion and CFO Anat Ashkenazi flagged that 2027 will “significantly increase” beyond that. Meta moved its range to $125–145 billion from $115–135 billion and gave back roughly 6% in after-hours trading on the print. Amazon committed approximately $200 billion. Apple disclosed $65 billion. The combined 2026 capex commitment across the five names now tracks the high end of consensus.

The headline is not the number. The headline is what the number contains. Multiple CFOs explicitly attributed a portion of the increase to component pricing rather than capacity expansion, with HBM memory called out by both Meta and Microsoft. The constraint has shifted: GPU supply has eased, memory has not. That changes the substrate ranking inside Compute.

NVDA closed Friday at $198.45, having printed an all-time high of $216.61 on April 27. The 8.4% pullback in five trading days is the largest one-week move in the name in months. The SOX, by contrast, kept rising. Compute is broadening: when the leader gives back and the index advances, capital is reallocating within the substrate, not leaving it.

The 76-point gap to the SOX from the inaugural reading widened to 77 points this week. The FNC-1 vs SOX spread is the more informative number than the basket level itself, since the basket is rebased weekly in v0.1 and the spread is computed on the same window each run. The substrate diversification is doing its work.

II. Belief

The Belief Index reads 52 this week, down from 55 at the April 27 reading. Three of the four panel components shifted in the same direction.

III. Read

The capex confirmation arrived on schedule. Three of four CFOs raised their 2026 guides on April 29. The structural thesis behind the FNC-1, that capital is being deployed across the four substrates at scale, is harder to dispute than it was a week ago.

The interesting move is internal to the panel. NVDA hit an all-time high the day Issue 005 published and is down 8% since. The SOX kept rising. Capital is rotating within Compute, not exiting it. That kind of internal differentiation becomes legible only on a multi-stock basket, not on a single-name read.

Belief moved in a coordinated direction. Three of four components shifted away from acceleration: AGI conviction fell seven points, OpenAI IPO conviction fell six, bubble-burst conviction rose three. Only GPT-6 firmed, by ten points to 90%, but a near-certain product release is a different kind of belief from “this is structurally working.” The composite Index of 52 understates the panel-level shift, since the GPT-6 firming partially offsets the three weakening signals.

The signal worth naming is what Issue 005 called the dominant belief: “this is not a bubble.” That conviction softened this week. Three points on a noisy market is not a regime change. But the direction is the data. Capex is being confirmed at unprecedented scale, and at the same time the prediction-market panel is becoming marginally more cautious about the cohort doing the spending. If both readings hold through Q2 earnings, capital deployment is outrunning capital realization for longer than the cohort assumed when it raised at peak. That is what the FNC-1 vs SOX gap is positioned to surface.

IV. What this measures, what it does not

The Belief Index is a snapshot of one venue's positioning, weighted by FP1's view of which markets matter for the AI transition. Individual components will be wrong. The aggregate, over time, is the signal.

The FNC-1 Proxy is a measurement instrument, not an investment vehicle. When divergence between FNC-1 and the SOX widens or compresses, that is data. The Belief Index helps frame what the divergence means.

Both instruments fail openly. NCB-003 specifies the falsification triggers.

V. Cadence

R-006 is the first Reading under the new cadence. The Capital and Belief panel will run every Monday. The longer-form State of the Transition Briefing returns Thursday, May 14 (B-001) with a Radar delta and the first substrate sub-index breakdown.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through May 1, 2026

- Microsoft Q3 FY2026 earnings press release, April 29, 2026

- Alphabet Q1 2026 Form 8-K, April 29, 2026

- Meta Platforms Q1 2026 Form 8-K, April 29, 2026

- Amazon Q1 2026 earnings release, April 30, 2026

- Polymarket — OpenAI achieves AGI before 2027

- Polymarket — GPT-6 released by Dec 31, 2026

- Polymarket — OpenAI IPO by Dec 31, 2026

- Polymarket — AI bubble burst by Dec 31, 2026

Capex was confirmed at scale.

Belief softened in coordinated form.

The cohort doing the spending is being repriced.

The instruments record both. The divergence is the read.