On Friday the U.S. stock market closed at another record high, its ninth straight winning week, and for once the chip stocks were not the ones leading. The Dow ran out front on the strength of Microsoft, IBM, and Salesforce, and Dell had its best day on record after a blowout quarter. After two years of a market that moved mainly when semiconductors moved, the rally looked like it was finally spreading out.

FNC-1, our index of the seven companies actually building the AI buildout, did not spread out with it. The Belief Index, a read on how convinced the betting markets are that the boom keeps going, barely moved at all. The week's record was real, and it happened almost entirely outside the part of the market this Reading watches most closely.

Picture the chief investment officer who has spent the spring waiting for permission to rotate out of semiconductors into the rest of the buildout, and who read Friday's record close as the all-clear. This Reading is for that decision. The instrument's answer is not the one the headlines implied.

I. Capital

Capital did broaden this week. It just broadened everywhere except where the buildout lives.

The record came on Friday, May 29, when the S&P 500 closed at 7,580 for a ninth consecutive weekly gain and all three major indexes hit fresh highs. The leadership was unusually wide. Dell jumped about 33%, its best session on record, after a beat-and-raise. IBM rose more than 11% and Salesforce more than 9%. Morgan Stanley's Skelly called the market's concentration in semiconductors, hardware, and power “extreme,” said it was now better to hold those names than add to them, and reached for a mid-1990s comparison, when chip outperformance stalled and the rest of the market caught up.

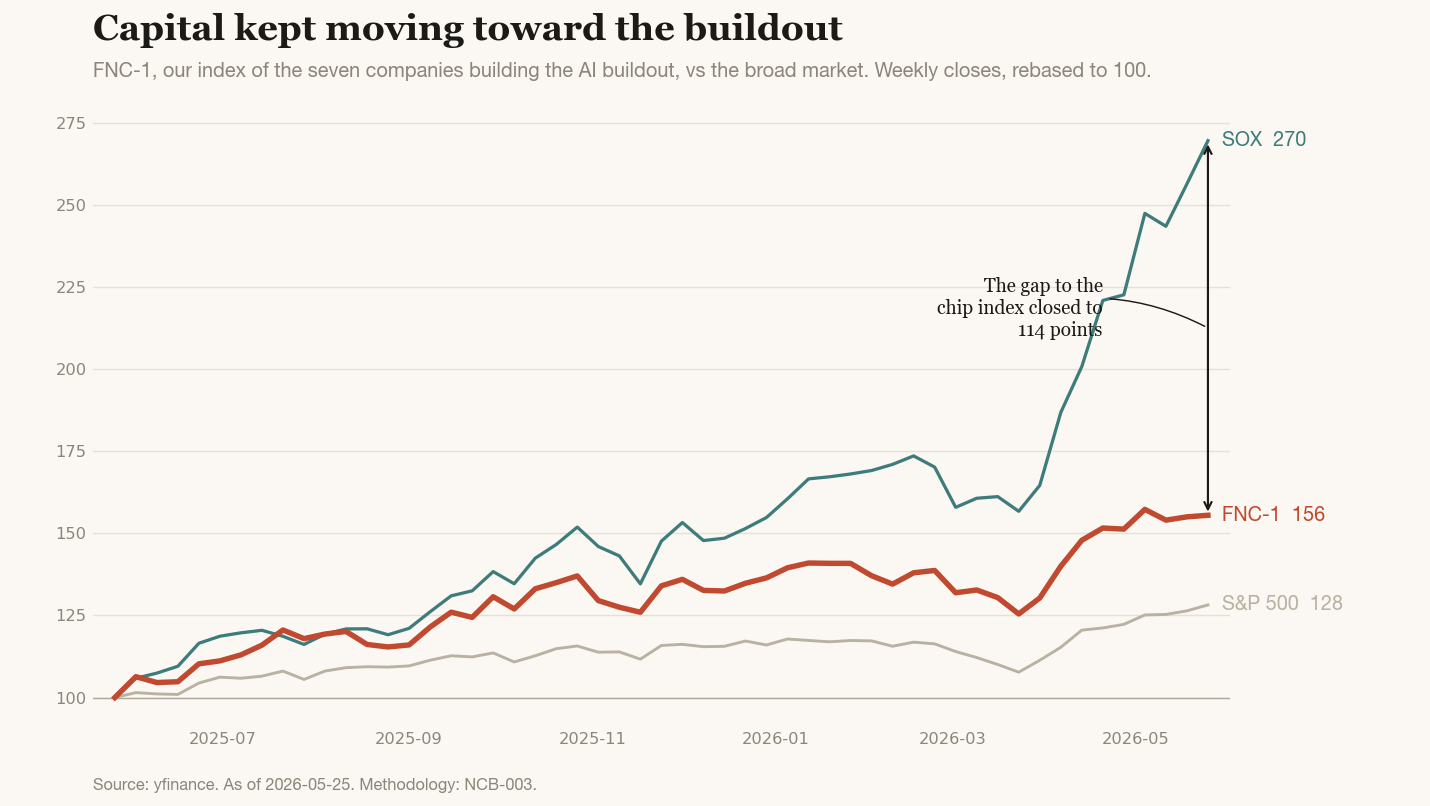

The instrument tells a different story than the indexes. The FNC-1 Proxy reads 155.5, up about 56% over the trailing twelve months. The Philadelphia Semiconductor Index, the benchmark for the chip complex, reads 269.6, and the S&P 500 reads 128.2, each rebased to 100 a year ago. The broad market made its record this week. The diversified buildout basket did not.

The four-substrate decomposition shows why. FNC-1 spreads its weight across compute, energy, the frontier labs, and biology. This week compute reads 188 against the basket's 156, the labs 160, energy 150, and biology 86, the only substrate lower than it was a year ago. The basket's strength is not broad. It is one layer deep, sitting closest to the chips, while the substrate furthest from them is in the red.

Even the breadth inside semiconductors was breadth inside compute. Nvidia spent the week in Taipei, hosting Jensen Huang's annual trillion-dollar dinner, while the sharp stock move came from elsewhere in the chip complex: AMD finished May up about 46%. The chip index pulled further ahead on more chip names, not on the rest of the buildout joining in.

The gap between FNC-1 and the chip index is the cleaner signal than either level, because the basket is rebased each week in this version of the instrument. That gap widened to about 114 points, from roughly 101 last week and about 90 the week before. Three readings, three steps wider. The chip complex is not just leading the buildout. It is pulling away from it.

II. Belief

The Belief Index reads 58 this week, unchanged from last week's reading. After last week's 45-point repricing in the OpenAI IPO market, the surprise this week is that nothing moved.

III. Read

Last week's Reading named a dominant frame: capital concentrating into compute while the exits open. This week tested it against a broad-market record, and the frame held. The catch-up everyone called did happen, but it happened in the index, not in the buildout. The S&P made a new high while the gap between the diversified basket and the chip index widened for a third straight reading. Record highs are not the same as a broadening buildout.

This is the reading a single Nvidia chart or the chip index alone cannot give you. Watch only the SOX and this was a strong, broadening week. Watch the four-substrate basket and the strength is one substrate deep: compute up 88% on the year, biology down 14%, the two ends of the buildout moving in opposite directions. The instrument exists to surface exactly this. Inside the buildout, leadership is narrowing, not widening.

The belief panel barely moved, and that stillness is the signal. Last week's IPO repricing could have been a one-week spike that gave itself back. It did not. The market still puts the odds of a public AI listing this year at better than two in three, and it firmed its conviction the cycle holds even into a week of open bubble warnings. The belief that the exits are opening is now a settled position, not a fresh reaction.

So capital is narrowing while belief holds firm, and one of them is early. The first real test arrives within days. SpaceX's public prospectus is on file, and its roadshow is reported to begin the week of June 4 with pricing targeted for June 11. That is the first time the exit-window thesis meets an actual public-market price rather than a prediction-market odds line. If the diversified buildout keeps lagging while the exits open on schedule, the question for the next month is not whether the boom is real. It is whether the market is paying for all four substrates or just the one nearest the chips.

IV. What this measures, what it does not

The Belief Index is a snapshot of one venue's positioning, weighted by FP1's view of which markets matter for the AI transition. Individual components will be wrong. The aggregate, over time, is the signal.

The FNC-1 Proxy is a measurement instrument, not an investment vehicle. When the gap between the basket and the chip index widens or compresses, that is data. The Belief Index helps frame what the gap means.

Both instruments fail openly. NCB-003 specifies the falsification triggers, and a spread that has widened three readings running is a claim that next week's data can check.

V. Cadence

The Capital and Belief Reading runs every Monday. The longer-form State of the Transition Briefing returns Thursday, June 11 (B-003), with the Radar delta, the full substrate sub-index decomposition this Reading only gestured at, and a first read on whether SpaceX's pricing moved the exit-window markets.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through May 25, 2026

- CNBC, stock market news for May 29, 2026 (record closes; S&P 500 at 7,580; Dell up about 33%; Micron and Qualcomm higher)

- TheStreet, Stock Market Today, May 29, 2026 (Morgan Stanley’s Skelly on extreme concentration and the mid-1990s parallel; IBM and Salesforce gains)

- GuruFocus, May market highlights (AMD up about 46% in May; monthly index gains)

- Digitimes Asia weekly roundup, June 1, 2026 (Nvidia at GTC Taipei; Huang’s trillion-dollar dinner, May 28; Taiwan adds 5.2 GW of gas capacity)

- NVIDIA Newsroom (TSMC and Foxconn announcements, May 31, 2026)

- Investing.com, “The Trillion-Dollar IPO Test: SpaceX and OpenAI” (SpaceX S-1 public May 20; roadshow reported the week of June 4; pricing targeted June 11)

- Polymarket — OpenAI IPO by Dec 31, 2026

- Polymarket — AI bubble burst by Dec 31, 2026

- Polymarket — GPT-6 released by Dec 31, 2026

- Polymarket — OpenAI achieves AGI before 2027

- State of the Transition Reading R-008 (May 25, 2026) and Briefing B-002 (May 28, 2026)

Methodology: NCB-003: FNC-1, the Novacene Composite.