On Friday, about a trillion dollars came off the table in a single session, and nearly all of it came out of the companies that make the chips behind the AI boom. The trigger was not a bad quarter. Broadcom had just posted the best one in its history, and the market sold it anyway.

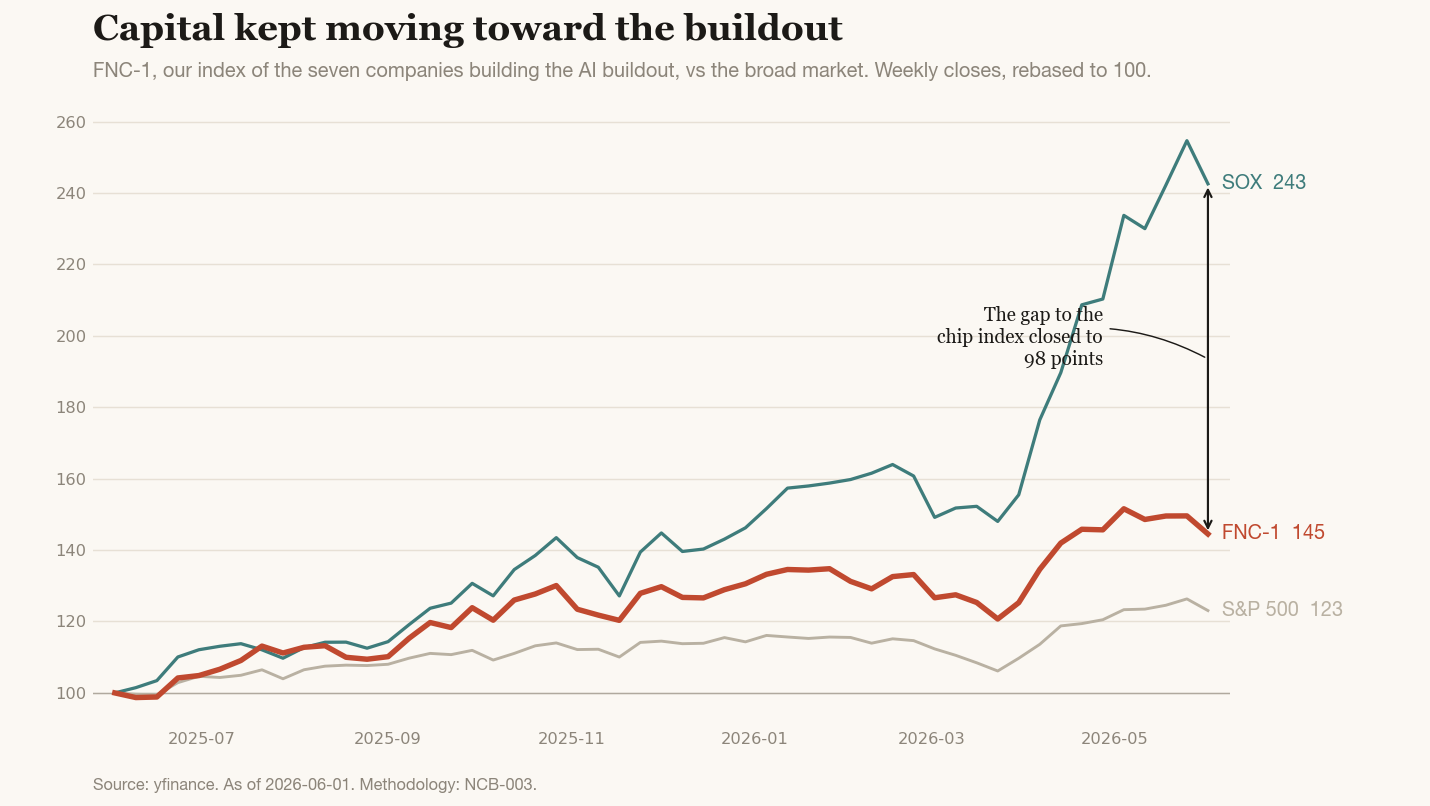

FNC-1, our index of the seven companies actually building the AI buildout, tracks capital across four substrates: compute, energy, the frontier labs, and biology. The Belief Index, a read on how convinced the betting markets are that the boom keeps going, tracks whether conviction holds. For three weeks this Reading watched the chip complex pull away from the rest of the buildout. This week the chip complex broke, and the instrument shows the break mostly missed the two compute names the basket holds.

Picture the allocator who saw Friday's headlines, “AI chip crash, worst day since April,” and assumed the Nvidia position at the center of the book had just cracked. This Reading is for that decision. The rout was real, and it landed hardest on chips this basket does not hold.

I. Capital

The chip index had its worst week since early 2025, and the diversified buildout basket fell with it, but less. The gap between them, which had widened for three straight readings, snapped shut, because the names that broke are mostly not the names this basket holds.

The week opened at records, with the S&P 500 above 7,600 and a fresh Dow high midweek. Then Broadcom reported after the close on June 3: record revenue of $22.19 billion, up 48%, with AI chip revenue of $10.8 billion, up 143%. But CEO Hock Tan left the full-year AI target unchanged, the raised forecast the market wanted, and said Broadcom would now sell custom chips only. The stock fell about 12% after hours. By Friday, June 5, the Philadelphia Semiconductor Index had dropped 5.21% in a single session, its worst since early 2025, with Broadcom, Marvell, Micron, AMD, and Intel all down sharply.

FNC-1 reads 144.5, up 44.5% over the trailing twelve months and down about 7% on the week. The Philadelphia Semiconductor Index, the benchmark for the chip complex, reads 242.6, up 142.6% on the year but down about 10% on the week. The S&P 500 reads 123.1. Each is rebased to 100 a year ago. Source: yfinance, Polymarket Gamma API. Methodology: NCB-003.

What broke was not demand, and it was not the basket's compute. Broadcom, Marvell, and Micron sit in the chip index. None sit in FNC-1, whose compute substrate is Nvidia and ASML, and that substrate fell only about 3% against the chip index's 10%. The rout was concentrated in the merchant and memory names this instrument was built to look past.

Nvidia is the cleanest illustration. It fell almost 6% on Friday and still finished the week close to flat, because the same complex that sold Broadcom's guidance had bid Nvidia's own new PC processor days earlier.

The gap between FNC-1 and the chip index is the cleaner signal than either level, because the basket is rebased each week in this version of the instrument. That gap had widened for three straight readings, to about 114 points last week. This week it compressed to about 98. It compressed not because the basket rallied, but because the chip index fell on names the basket does not hold. Three readings of widening, reversed in the week the chips finally cracked.

II. Belief

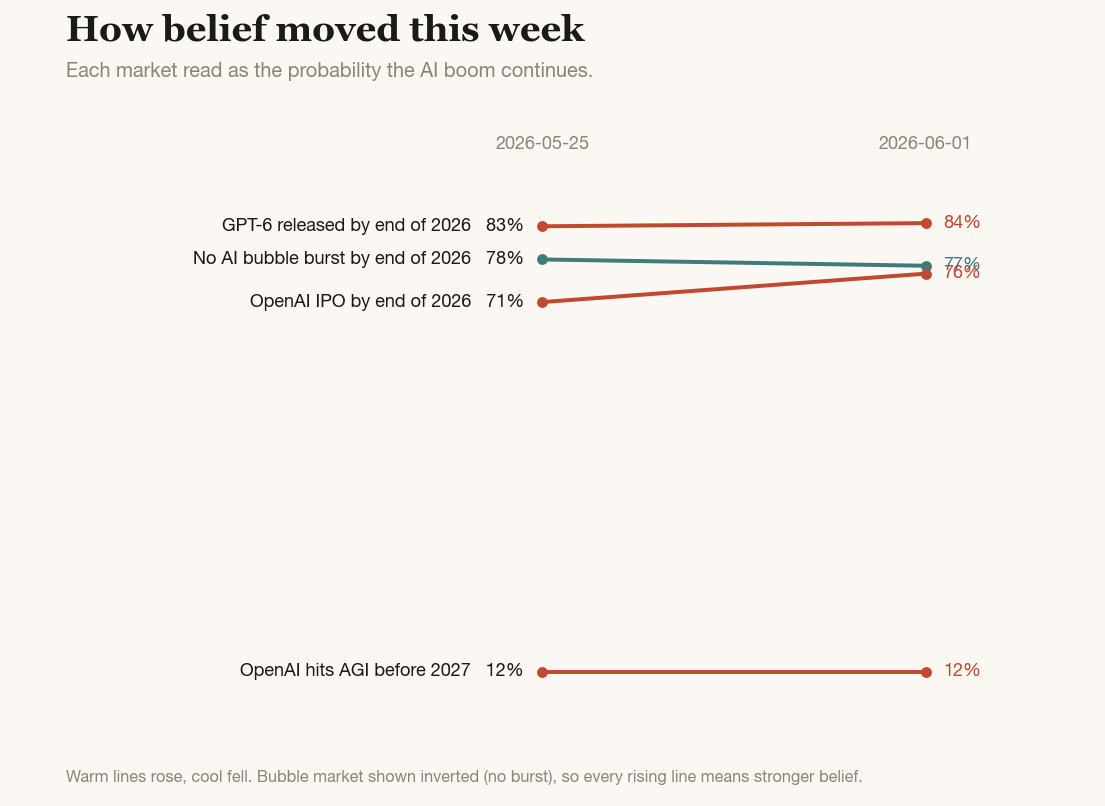

The Belief Index reads 59 this week, essentially unchanged from 58 at last week's reading.

III. Read

Last week's Reading named a dominant frame: the chip complex was pulling away from the rest of the buildout, and the gap to the SOX had widened three readings running. It closed on a question, whether the market was paying for all four substrates or just the one nearest the chips. This week the chips cracked, and the answer arrived with a twist. The chip index broke. The two compute names this basket holds did not.

This is the reading the chip index alone cannot give you. Watch the SOX and Friday was a 10% week. Watch the four-substrate basket and the same week is a 7% pullback, because the names that fell hardest, Broadcom and Micron and AMD, are names this instrument was built to exclude. Compute fell only about 3%. The basket's real damage was elsewhere: biology, a single volatile name, fell about 30% on the week and did most of the work dragging the basket lower. The chip story and the basket's worst substrate had nothing to do with each other.

Belief did not move with the tape. The Belief Index held at 59 through a week of bubble warnings and a trillion-dollar drawdown, and the one market that did move, OpenAI's IPO odds, moved up. The exit window the last several Readings have tracked did not pause for the selloff. SpaceX set a fixed price of $135 a share, targeting about $75 billion at a valuation near $1.75 trillion, the largest listing on record, with pricing due June 11 and a Nasdaq debut June 12. The chips broke on Friday. The exit window opened on schedule the same week.

So the week that looked like the boom cracking was narrower than the tape implied. The chip index fell hard, on names the basket does not hold. The compute leaders held, belief held, and the exit window firmed. The gap compressed because the SOX fell to meet the basket, and the next several weeks will show whether that is the chip complex calming down or the rest of the buildout starting to follow it lower. SpaceX's first print on June 12 is the immediate test, the first time the exit thesis meets a real market price rather than a prediction-market line.

IV. What this measures, what it does not

The Belief Index is a snapshot of one venue's positioning, weighted by FP1's view of which markets matter for the AI transition. Individual components will be wrong. The aggregate, over time, is the signal.

The FNC-1 Proxy is a measurement instrument, not an investment vehicle. When the gap between the basket and the chip index widens or compresses, that is data. This week it compressed to about 98 points after three readings of widening, and the compression carries the weight the widening did.

Both instruments fail openly. NCB-003 specifies the falsification triggers. A spread that widened three readings running and then reversed in a single week is a claim the next several readings can check.

V. Cadence

The Capital and Belief Reading runs every Monday. The longer-form State of the Transition Briefing returns Thursday, June 11 (B-003), with the Radar delta, the full four-substrate decomposition this Reading only gestures at, including the biology move, and a first read on whether SpaceX's pricing moved the exit-window markets.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through June 1, 2026 (week ending June 5)

- CNBC, stock market news for June 1–2, 2026 (S&P 500 first close above 7,600; Nvidia higher on a new PC processor; Alphabet down about 4% after an $80 billion stock sale to fund its AI buildout, including a $10 billion Berkshire Hathaway investment)

- Broadcom Inc. Form 8-K, Q2 FY2026 results, June 3, 2026 (revenue $22.19 billion, up 48%; AI semiconductor revenue $10.8 billion, up 143%; full-year AI target left unchanged; fiscal 2027 AI target reiterated above $100 billion)

- Quartz, Broadcom Q2 2026 earnings (a beat without a raise; Hock Tan’s shift to custom AI chips only; Google to draw on multiple suppliers)

- TheStreet and Trading Economics, Stock Market Today, June 5, 2026 (Philadelphia Semiconductor Index down 5.21% in a single session, its worst since early 2025; Nasdaq down 4.2%, worst since April 2025; S&P 500 down 2.6%; Broadcom, Marvell, Micron, AMD, and Intel all down sharply; Nvidia down 5.93%)

- CNBC and Reuters, SpaceX IPO coverage, June 3, 2026 (fixed price of $135 per share; about $75 billion raise; valuation near $1.75 trillion; pricing targeted June 11; Nasdaq debut June 12 under ticker SPCX; Goldman Sachs lead underwriter)

- Wall Street IPO and concentration debate (Bank of America’s Michael Hartnett on technology’s weight in the S&P 500 breaching the 48% threshold; Michael Burry’s expanded AI short positions)

- Polymarket — OpenAI IPO by Dec 31, 2026

- Polymarket — AI bubble burst by Dec 31, 2026

- Polymarket — GPT-6 released by Dec 31, 2026

- Polymarket — OpenAI achieves AGI before 2027

- State of the Transition Reading R-009 (June 1, 2026) and Briefing B-002 (May 28, 2026)

Methodology: NCB-003: FNC-1, the Novacene Composite.