Two weeks ago this Briefing told you the buildout runs on three clocks that do not agree: leases signed for fifteen years, power that takes up to eight to arrive, chips that are old in three. That was the structure. This fortnight, the bill for it showed up.

Broadcom posted the best quarter in its history and the market sold it anyway, because the company would not promise more. The chip index had its worst day in over a year. Then inflation came in at a three-year high, oil pushed toward $90 on a war that will not stay paused, and the index that tracks the buildout's actual builders slid to its weakest tape in five weeks. And into exactly that weather, tonight, SpaceX prices the largest stock listing ever attempted.

What changed is not the buildout. The leases held, the capital budgets held, the builders' shares held better than the chips around them. What changed is the price of waiting. The desks below measure that price; the ledger at the end records what we are willing to be wrong about.

This Briefing tracks the structural shift from an extractive, human-bottlenecked industrial order to one organized around machine intelligence, adaptive governance, and new forms of capital allocation. The dimension this issue illuminates is carry: what it costs to hold the long side of the duration mismatch while the short side churns. B-001 named the counterparty. B-002 named the clocks. B-003 names what the clocks cost when money stops being patient.

Three measured facts set the fortnight. Broadcom reported record fiscal Q2 revenue of $22.19 billion, up 48%, with AI semiconductor revenue of $10.8 billion, up 143%, then left its full-year AI target unchanged, and the stock fell roughly 12% after hours, per the company's June 3 release and the desks that covered it. Two sessions later the Philadelphia Semiconductor Index fell 5.2%, its worst single day since April 2025, in a session that took roughly a trillion dollars off the market, per TheStreet and Trading Economics. And on June 10, the morning before this Briefing published, May CPI printed at 4.2%, the highest in three years, with WTI crude settling near $90 as US strikes on Iran resumed, per Bloomberg. The S&P 500 closed at a five-week low.

The Briefing's structural read this fortnight: the market did not reprice the buildout. It repriced the patience that funds it. The leases, the capex commitments, and the pre-leasing rates that B-002 documented are unmoved. What moved is the cost of carrying them, the willingness of the tape to pay for capacity stories without monetization proof, and, as of tonight's SpaceX print, the first real market test of whether the exit window stays open in bad weather.

Radar Delta

This Briefing opens three new signals on the cost-of-carry cluster, reframes one, hardens one, and reports the duration cluster from B-002 unchanged pending its next scheduled checks.

NewMacro re-entry as a cost-of-carry constraint. May CPI printed at 4.2% on June 10, a three-year high, per TheStreet's same-day market report. WTI crude settled near $90 as the US resumed strikes on Iran following the downing of an Apache helicopter over the Strait of Hormuz, per Bloomberg and NBC News reporting. The VIX jumped 34% in the June 5 session and held above 20 through the week. None of this is an AI signal by itself. It becomes one through the duration channel: B-002 established that the cycle's commitments are decade-dated and rigid, which means the discount rate applied to them is now a live variable rather than a footnote. A buildout financed at 2024 patience and 2026 rates are two different assets. Maturity: Active. Risk: High. Next check: June FOMC and the July CPI print.

NewThe financing channel as the buildout's load-bearing layer. Alphabet completed an $80 billion stock sale early in the fortnight to fund its AI buildout, including a $10 billion Berkshire Hathaway investment, per CNBC's June 1–2 market coverage. A Meta secondary offering was named among the triggers of the June 5 rout, per TheStreet. Hyperscaler 2026 capex guidance locked in the Q1 cycle at roughly $650 to $725 billion, with capital intensity at 45 to 57% of revenue, and sector research citing Morgan Stanley and J.P. Morgan projects roughly $1.5 trillion of new technology debt issuance over three years. When capex runs past internal cash generation, the marginal builder of the buildout is the capital markets, and the macro entry above just repriced that builder's terms. Maturity: Active. Risk: High. Next check: issuance calendars and hyperscaler CDS spreads, the credit thread the Readings have carried since R-006.

NewThe exit window meets a live tape. SpaceX prices after tonight's close at a fixed $135 per share, targeting roughly $75 billion at a valuation near $1.75 trillion, the largest listing on record, with a Nasdaq debut June 12 under SPCX, per Reuters. Reported structure: roughly 3% initial float and an unusually large retail allocation near 30%. A reported Nasdaq-100 fast entry roughly fifteen sessions after listing, with an estimated $22 to $27 billion of mechanical index demand, circulates in secondary coverage and is treated here as unverified. The print is the first time the exit-window thesis the Readings have tracked since R-008 meets a real market price rather than a prediction-market line, and it arrives in the worst tape of the cycle's recent run. Maturity: Active. Risk: Medium. Next check: first-fortnight trading through June 26.

ReframedThe narrative premium, now repricing in real time. Broadcom's quarter was a record on every reported line and the stock was sold for the absence of a raised forecast, with CEO Hock Tan additionally narrowing the business to custom AI chips only, per the June 3 release and Quartz's read. The fortnight's selling concentrated in merchant and memory names that FNC-1 excludes; R-010 measured the compute substrate down only about 3% against the chip index's roughly 10% week. The reframe: the premium is compressing from the edges inward. Results no longer carry guidance-free valuations, and the market has begun demanding monetization proof before extending the multiple. This is the verification regime FP1's framework predicts, arriving through the tape rather than through a filing. Maturity: Active. Risk: Medium. Next check: whether beats-without-raises continue to be sold through the July reporting cycle.

HardenedHardware useful-life and the depreciation debate. The gate B-002 set, a further useful-life shortening or a write-down at a top-five hyperscaler, did not trigger this fortnight; the next disclosure window is the Q2 10-Q cycle in July. The instrumentation improved. Research Affiliates published a formal net-versus-gross framework: under a two-year economic life, less than 20% of gross capex adds to productive capital, and even under seven years the ratio stays below 60%, implying that more than half of 2026's roughly $650 billion of hyperscaler capex replaces obsolete hardware rather than expanding capacity under plausible assumptions. The argument has moved from a short-seller's thesis to peer-grade research with stated sensitivities. Maturity: Active. Risk: High. Next check: Q2 10-Q useful-life disclosures, July–August.

HeldThe duration cluster, unchanged pending scheduled checks. No new transformer lead-time, interconnection, or siting reads surfaced this fortnight. The five B-002 signals hold at Active with their next checks unchanged: the Wood Mackenzie Q2 2026 lead-time survey, the LBNL 2026 queue update, and the H100 secondary-rental floor near $2.00 per hour on the value-cascade watchlist.

Capital sub-indices

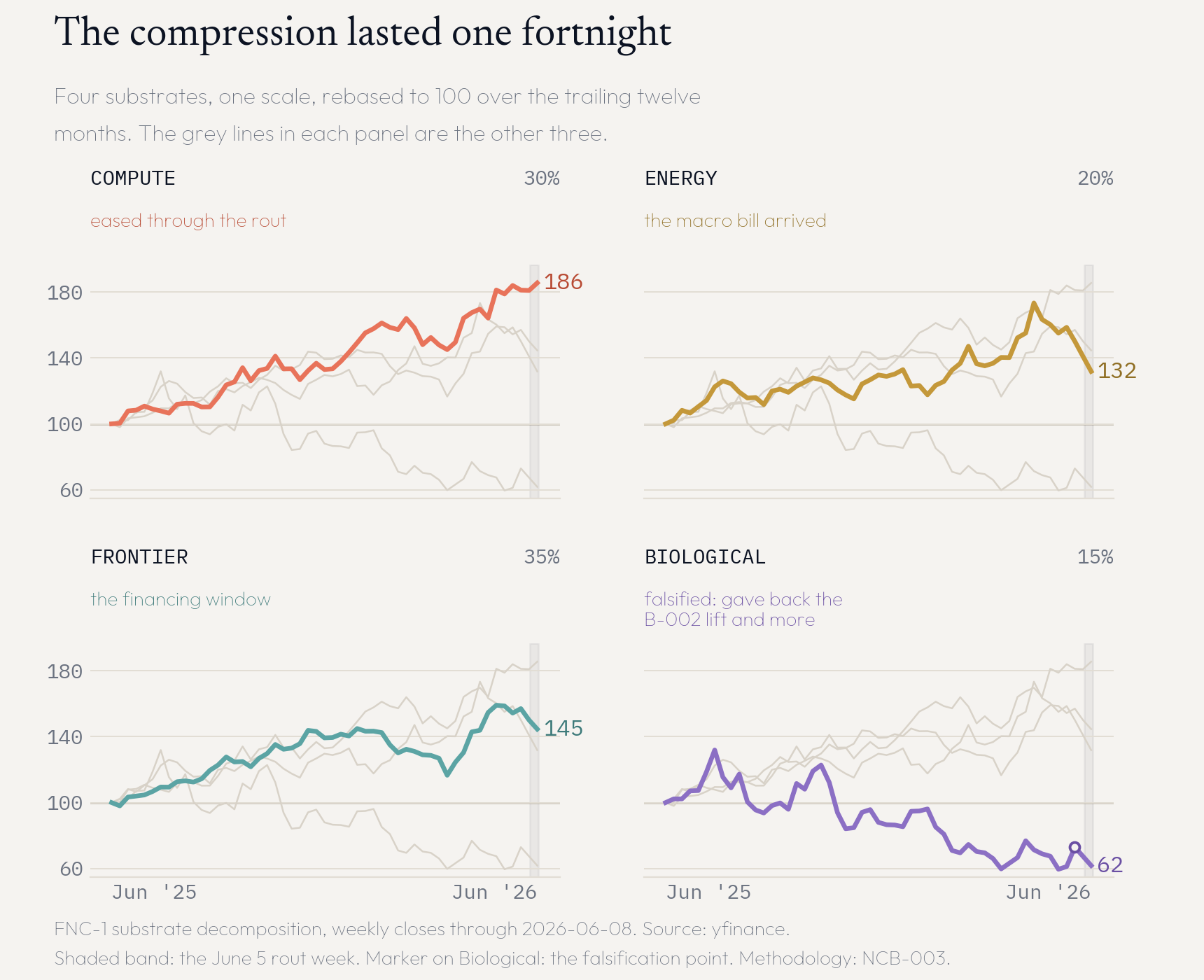

The fortnight's print is a divergence: the laggard broke down while the leaders eased. B-002 closed on a compression, the four substrates moving toward each other for the first time in the instrument's run. The compression lasted one fortnight. The leader-laggard spread re-widened from 111 points to 124, and it widened from the bottom: Biological gave back its entire B-002 lift and more, while the three leading substrates absorbed the worst chip session in over a year with single-digit declines. The composite's last weekly print, per R-010, reads 144.5 against the SOX at 242.6 and the S&P 500 at 123.1, with the gap to the chip index compressed to roughly 98 points because the chip index fell to meet the basket.

Compute (30% weight). The constituents are NVDA and ASML. The substrate closed near 186, easing about 1% from the 187 print in B-002 through the worst chip week since early 2025. The damage concentrated in merchant and memory names the instrument was built to exclude: Broadcom, Marvell, Micron, AMD, and Intel led the June 5 decline, and the same names led the June 8 rebound, with Micron up nearly 10% and Intel up 11%. Nvidia finished the rout week close to flat and added 2.3% on June 8 on a memory partnership with SK Hynix for its AI-factory buildout, per CNBC. The leader-within-leader read from R-006 and R-007, memory as the binding constraint behind the substrate's lead, gained a data point: the constraint's suppliers are now where the volatility lives.

Energy (20% weight). The constituents are CEG and GEV. The substrate closed near 132, the largest absolute pullback among the leaders for the second consecutive issue. The fortnight added a genuinely two-sided macro input: oil near $90 raises the cost of the gas-turbine bridge that backstops behind-the-meter generation, while simultaneously hardening the scarcity premium on already-interconnected baseload, which is the right-of-way logic B-002 named. The PJM curtailment framework and the CEG structural position are unchanged. The pullback remains a market move, not a thesis move, but it is now a market move with a macro bill attached.

Frontier (35% weight). The constituents are MSFT and GOOGL. The substrate closed near 145, the middle of the leader pack. The fortnight's signal here is not price but plumbing: Alphabet sold roughly $80 billion of stock to fund its buildout, with Berkshire Hathaway taking $10 billion, and traded down about 4% on the dilution, per CNBC. The heaviest weight in FNC-1 is now the cleanest single window onto the financing channel: a frontier lab choosing equity issuance at scale, at these prices, to keep the capex book funded. Whether that reads as confidence or as strain is exactly the divergence logged below.

Biological (15% weight). The constituent is RXRX. The substrate closed near 62, down roughly 19% over the fortnight, after extending its B-002 lift into early June and then giving all of it back and more in the rout week, when it fell about 30%. The proximate record: a June 4 pivot top followed by five consecutive down sessions, a $3.04 close on June 10 within sight of the $2.77 52-week low, and the standing overhangs of a 60% Q1 revenue miss reported May 6, a $300 million at-the-market dilution program, and founder Chris Gibson's decision not to seek board re-election after June, per Zacks, Trefis, and Simply Wall St coverage. B-002 stated its condition plainly: the broadening read was supported only if the move survived the next two weeks. It did not. The falsification is logged in the Implications and the Ledger.

Leader: Compute (186). Laggard: Biological (62). Leader-laggard spread: 124 points, re-widened from 111 in B-002. Composite-to-SOX spread: roughly 98 points per R-010, compressed from about 114, because the chip index broke on names the basket does not hold. The decomposition's read this fortnight: the buildout's core held, its speculative edge cracked, and its biological frontier failed its own test.

Scenario Revision

B-002 opened a four-branch scenario tree on the duration mismatch. This is its first scheduled revision, and it begins with an admission: the tree had no exogenous branch. All four triggers were internal to the buildout, power, shells, hardware, demand, and the fortnight's stress arrived from outside, through inflation, oil, and a war premium. Rather than adding a fifth branch, the revision names the financing channel as the mechanism inside Branch D, which is where an exogenous squeeze becomes an endogenous outcome.

Branch A, power scarcity persists, 45 → 42. Nothing in the fortnight tested the power leg; the trim reflects only the mass transferred to D. The value cascade held, no queue or transformer relief surfaced, and the scarcity premium on interconnected baseload, if anything, hardened with oil near $90.

Branch B, obsolescence reaches the shell, 30 → 26. No stranded-shell evidence either way. The Research Affiliates net-versus-gross framework sharpens the silicon-side argument without touching the building-side question, which remains under-instrumented, exactly as Vera graded it in B-002.

Branch C, power delivery compresses, 15 → 12. No compression evidence this fortnight, and the macro entry cuts against it: a higher cost of capital slows, rather than accelerates, speculative generation and grid investment outside the hyperscalers' own balance sheets.

Branch D, demand cools, 10 → 20. The fortnight's move, and the revision's discipline matters here: lease demand did not cool. Pre-leasing, pricing, and capex books are intact. What changed is the visibility of the mechanism by which demand would cool, the financing channel. An $80 billion equity sale, a secondary offering in the rout's trigger mix, projected trillion-scale debt issuance, and a 4.2% CPI print together describe a buildout whose marginal dollar now has a market price. D doubles not because demand weakened but because the path from here to there stopped being hypothetical.

Correspondent Dispatches

ConfirmedBroadcom's fiscal Q2: revenue of $22.19 billion, up 48%, AI semiconductor revenue of $10.8 billion, up 143%, full-year AI target left unchanged, shares down roughly 12% after hours. Sourced to the company's June 3 Form 8-K and consistent across Quartz, CNBC, and TheStreet. The quarter is not in dispute. The sale of it is the data.

ConfirmedThe June 5 session: the Philadelphia Semiconductor Index down 5.2%, its worst single day since April 2025, the Nasdaq down 4.2%, roughly a trillion dollars off the market, the VIX up 34% and above 20. TheStreet and Trading Economics converge, and the figures are consistent with R-010's print.

ConfirmedThe macro turn: May CPI at 4.2%, a three-year high, on June 10; WTI settling near $90 as US strikes on Iran resumed; the S&P 500 at a five-week low. Bloomberg, TheStreet, and TipRanks converge on the same three drivers in the same session.

ConfirmedSpaceX prices after the June 11 close at a fixed $135 per share, targeting roughly $75 billion at a valuation near $1.75 trillion, debuting June 12 on Nasdaq as SPCX. Reuters, with the roadshow timeline corroborated across broker disclosures.

HighThe reported deal structure: an initial float near 3% and a retail allocation near 30%, roughly triple the norm. Multiply reported, but allocations settle only at pricing; treat the proportions as directionally solid and the precise figures as provisional until the final prospectus.

UnverifiedThe Nasdaq-100 fast-entry claim: inclusion roughly fifteen sessions after listing, with $22 to $27 billion of forced passive buying. The figure circulates in secondary coverage only. Index fast-entry rules make early-July review plausible; the dollar estimate has no primary source this desk has located. It is a tradable rumor, which is not the same thing as a fact.

UnverifiedThe “skeptical AI report” named in the June 5 trigger mix. TheStreet's session report cites strong payrolls, a skeptical AI report, and the Meta secondary as the drivers. The report's identity does not appear in the primary record this desk reviewed. A selloff trigger that cannot be sourced is itself a finding: some of Friday's move was narrative responding to narrative.

DisputedThat the fortnight's drawdown is evidence the AI cycle is breaking. The counter-evidence is specific: the rout concentrated in merchant and memory names FNC-1 excludes, the compute substrate fell about 3% against the chip index's roughly 10% week, the capex books and lease commitments B-002 documented are unmoved, and the June 8 rebound was led by the same names that broke. The fortnight confirms a repricing of the narrative premium. It does not yet confirm a repricing of the buildout. Those are different claims and they will resolve on different evidence.

Falsified this cycleB-002's biological broadening read. The condition was stated in the issue: the move was better-supported, conditional on surviving the next two weeks. The substrate fell roughly 30% in the rout week and sits near its 52-week low. The thread closes as specified. The methodology's longer prediction, that the cycle eventually broadens into Biological, stays on the Radar as a compass claim; the clock claim failed.

Falsification candidate to watch. Tonight's print. If SpaceX prices at $135 and holds above offer through its first fortnight while CPI sits at a three-year high, the claim that macro closes the exit window weakens materially. If it breaks below offer in week one, the financing-channel entry on this issue's Radar hardens from inference to observation. Either way, by June 26 the exit-window thesis has a market-priced answer for the first time.

Treat the rout as confirmed and the regime change as unverified. The spread between a falling tape and an unmoved capex book is where this fortnight's information lives.

The binding constraint of the fortnight is carry. B-001 named the counterparty, B-002 named the clocks, and the question this issue is forced to ask is who finances the gap between them, at what price, for how long. The duration mismatch was a physics problem: power arrives slower than leases commit and faster than hardware dies. As of this fortnight it is also a financing problem, because the entities holding the long side of the mismatch are now visibly funding it in the open market.

Name the actors. Alphabet sold roughly $80 billion of stock to fund its buildout and took a $10 billion check from Berkshire Hathaway, which is the most duration-tolerant capital in the market choosing the equity layer rather than the lease layer. Meta ran a secondary into the same week. Hock Tan posted the best quarter in Broadcom's history, declined to raise, and narrowed the firm to custom silicon only, which is a supplier electing certainty of a few large counterparties over breadth, the same counterparty concentration B-001 mapped, now chosen voluntarily from the supply side. And the hyperscalers as a cohort are running capital intensity of 45 to 57% of revenue against roughly $1.5 trillion of projected debt issuance. When capex outruns internal cash generation, the marginal builder of the buildout is the bond and equity market. Wednesday's CPI print repriced that builder's terms.

The scenario revision above carries the structural change: the tree gets no fifth branch, but Branch D doubles to 20% because its mechanism is now observable. Note what the revision does not do. It does not treat a volatility week as a regime. The adversarial read against this issue's framing is strong and worth stating at full force: Iran premiums and one hot CPI print are weather, not climate. The duration thesis is about whether powered shells hold value across hardware generations, and nothing in a four-session drawdown speaks to that question at all. If the tape recovers, the FNC-1-to-SOX gap re-widens within three Readings, and SpaceX trades through its offer with a passive bid behind it, then B-003's macro entry was noise and this Briefing over-weighted a bad week. That failure condition is logged in the Ledger with a date on it.

Phase-transition candidate: tonight's print, treated correctly. SpaceX is not a space story for this Radar. It is the single highest-information observation available this quarter on risk appetite for long-duration assets, because it is the largest such asset ever priced, pricing on the worst tape of the run, with a structure, a 3% float, a retail tranche, a rumored index bid, engineered to succeed. If an offering engineered this thoroughly cannot hold $135, the financing channel is tighter than any spread currently shows. If it holds, the channel is open and the buildout's funding bridge stands, at a higher toll.

The fortnight repriced the lender, not the lease. Watch who still gets term, and at what price.

The archetype at work this fortnight is the Bridge, and the bridge under load is not made of steel. Every transition builds two structures at once: the asset itself, and the financing architecture that carries commitments across the gap between spending and earning. The asset is concrete, transformers, and silicon. The bridge is paper, leases, bonds, secondaries, and listings. B-002 examined the asset. This fortnight, the weather arrived on the bridge.

The precedent is September 1873. Jay Cooke and Company had financed the Union's war and then took on the Northern Pacific Railway, selling bonds against a road that was real, toward demand that was real, through country that would in time carry traffic for a century. What failed was not the railroad. What failed was the placement: when money tightened in the autumn of 1873, Cooke could no longer sell the next tranche of paper, his house suspended on September 18, and the panic that followed closed the New York Stock Exchange for ten days. The builders had not misjudged the demand for rail. They had misjudged whether the bridge of paper carrying it was rated for weather.

The mechanics transfer with uncomfortable precision. A buildout whose capital intensity runs past internal cash flow is, structurally, a continuous placement of new paper: equity sales, debt programs, and, tonight, the largest single listing ever attempted, walking onto the bridge in the first storm of the cycle. Demand for compute is not the question, exactly as freight demand was not the question in 1873. The question is whether the financing structure holds when patience gets a price.

But 1873 carries a second lesson, and it is the one that matters for orientation. The panic did not end the railroad age. Track mileage resumed within the decade, and the road Cooke could not finance was completed by others and used for a hundred years. What the panic changed was who owned the road. Completed, revenue-bearing track survived the squeeze and concentrated into stronger hands. Promises of track did not. The transition finished; the builders rotated. In every financing panic inside a real transition, the asset outlives the paper, and ownership migrates from those who needed the next placement to those who did not.

The first-principles imperative for the institutional reader paid to be right about the Transition: separate your exposure to the buildout from your exposure to the bridge. An asset already earning against its commitments crosses on its own weight. An asset that requires the continuous placement of new paper is not a position on the buildout. It is a position on the bridge, and the bridge was just asked to carry its first storm. The grades on whether it holds belong to Vera's desk; the orientation is older than the cycle.

Demand builds the road. The bridge of paper decides who finishes it.

Implications

Falsification first: B-002's biological broadening read failed its own condition. The issue stated that the substrate's lift was better-supported only if the move survived two weeks. It fell roughly 30% in the rout week, on a revenue miss, a dilution overhang, and a founder exit, and sits near its 52-week low. The thread is closed as a clock claim; the compass claim, that the cycle eventually broadens into Biological, remains on the Radar with no current evidence in its favor. The leader-laggard spread re-widened to 124 points. We said what would falsify the read, and it did.

The premium is repricing before the buildout is. A record quarter sold for the absence of a raise is the market shifting from paying for capacity stories to demanding monetization proof, and the selling concentrated in the names furthest from verified deployment. Through the July reporting cycle, expect guidance, not results, to move prices. FP1's working read: this is the verification regime arriving through the tape, not the cycle breaking. The two claims separate cleanly on the gap data, which is why the gap is this fortnight's divergence crux.

The duration mismatch now has a carry cost, and the financing channel is the new leading indicator. Inflation at a three-year high and a war premium in oil raise the price of holding ten-to-fifteen-year commitments funded past internal cash flow. An $80 billion equity sale and trillion-scale projected debt issuance make the funding leg observable. Issuance calendars, secondaries, and hyperscaler credit spreads now join the 10-K useful-life disclosures as the filings-before-research watchlist.

Tonight's print is a regime test, not a space story. SpaceX pricing is the first market-priced observation on the exit-window thesis this publication has tracked since R-008, delivered by the largest long-duration asset ever listed, on the weakest tape of the run, with a structure engineered to succeed. Above offer through June 26, the financing bridge holds at a higher toll. Below offer in week one, this issue's financing-channel entry hardens from inference to observation.

Call Ledger

Every standing claim this issue is willing to be scored on, each with its falsifier and check date. Resolved calls are reported in the issue after their check date, hits and misses alike.

| Call | Claim | Falsifier | Check | Desk |

|---|---|---|---|---|

| CALL-2026-031 | SpaceX prices at $135 and closes its first fortnight above offer. | A close below $135 by June 26. | Jun 26 | Manticus |

| CALL-2026-032 | The FNC-1-to-SOX gap re-widens above 110 points within three Readings, confirming the rout missed the buildout's core. | Gap below 90 at R-013. | Jun 29 | Vera |

| CALL-2026-033 | A top-five hyperscaler shortens AI-hardware useful life again, or books a related impairment, by the Q2 10-Q cycle. Carried from B-002. | No revision in any Q2 10-Q. | Aug 14 | Vera |

| CALL-2026-034 | H100 secondary rental holds above $2.00 per hour, keeping the value cascade orderly. Carried from B-002. | A sustained print below $2.00. | Sep 30 | Manticus |

| CALL-2026-035 | The Biological substrate stays below 70 at B-004, keeping the broadening thread closed. | A recovery above 70 by June 25. | Jun 25 | Vera |

| DR-2026-004 | Divergence, open: is the drawdown regime information for the duration thesis? Resolves on the gap data and the SpaceX tape. | See record above. | Jun 22 | Vera |

Cadence

The standing Radar sits with the weekly Reading. The next Capital and Belief Reading runs Monday, June 15 (R-011), with the first SpaceX tape, the post-pricing read on the exit-window markets, and the first check on the gap call opened above. The next Briefing runs Thursday, June 25 (B-004), with the resolution of CALL-2026-031 and -035, the divergence record's first review, and the scenario tree carried forward.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through June 8, 2026

- Broadcom Inc. Form 8-K, fiscal Q2 2026 results, June 3, 2026 (revenue $22.19B, +48%; AI semiconductor revenue $10.8B, +143%; full-year AI target unchanged)

- TheStreet, Stock Market Today, June 5, 2026 (Nasdaq −4.18%, NDX −4.77%, VIX +34% above 20; trigger mix: strong payrolls, a skeptical AI report, Meta secondary; ~$1T single-session drawdown)

- Trading Economics / TheStreet, June 5, 2026 (Philadelphia Semiconductor Index −5.21%, worst session since April 2025)

- CNBC, stock market news for June 8, 2026 (chip rebound: Micron +10%, semiconductor ETF +6%; Nvidia +2.3% on SK Hynix AI-factory memory partnership; S&P 500 7,405.73)

- CNBC, stock market news for June 1–2, 2026 (S&P 500 first close above 7,600; Alphabet ~$80B stock sale to fund its AI buildout, including a $10B Berkshire Hathaway investment, shares −4%)

- TheStreet, Stock Market Today, June 10, 2026 (May CPI 4.2%, a three-year high; Dow −953 to 49,918.78; Nasdaq −1.98% to 25,169.50; renewed US strikes on Iran)

- Bloomberg, June 10, 2026 (S&P 500 at a five-week low, −1.6%; chip gauge −3.6%; WTI near $90; Iran strikes)

- Reuters and CNBC, SpaceX IPO coverage, June 3–9, 2026 (fixed price $135; ~$75B raise; ~$1.75T valuation; pricing after close June 11; Nasdaq debut June 12 as SPCX; ~3% initial float; ~30% retail allocation reported)

- Secondary IPO coverage, June 2026 (reported Nasdaq-100 fast entry ~15 sessions post-listing, est. $22–27B passive demand; treated as unverified)

- Research Affiliates, “When Will AI Be Both Powerful and Profitable?” (net-vs-gross capital formation; under a 2-yr life net-to-gross <20%, under 7-yr <60%; ~$650B 2026 hyperscaler capex per Bloomberg)

- Q1 2026 hyperscaler disclosures and sector research (2026 capex guidance ~$650–725B; capital intensity 45–57% of revenue; Morgan Stanley and J.P. Morgan est. ~$1.5T technology debt issuance over three years, as cited in sector coverage)

- Zacks, Trefis, Simply Wall St, and StockInvest coverage of Recursion Pharmaceuticals, May–June 2026 (Q1 revenue $6.47M vs ~$16M consensus; $300M ATM program; founder Chris Gibson not seeking board re-election; June 4 pivot top; $3.04 close June 10 vs $2.77 52-week low)

- State of the Transition Reading R-010 (June 8, 2026) and Briefing B-002 (May 28, 2026)

The commitments are long.

The patience just got a price.

Tonight, the bridge takes its first storm.

The Briefing tracks the system. The Radar holds the threads. The Ledger keeps the score.