The Read · 90 secondsThe Read

For six weeks the chip stocks ran ahead of the companies actually building AI, and the distance between them kept widening. This week the distance finally shrank. It shrank because the chips fell, not because the builders rose.

So here's the week in one line: the whole complex came down, the chips came down hardest, and the gap to the chip index closed for the first time in weeks, for the wrong reason. Underneath, belief in the boom slipped below 50 for the first time in the series, but it slipped on the timing bets, not on the odds of a crash. The instruments show both moves.

FNC-1, our index of the seven companies building the AI buildout (NCB-003), reads against the SOX, the chip index most people watch, and the S&P 500. Beside it sits the Belief Index, a read on how convinced the betting markets are that the boom keeps going. When the two pull apart, the divergence is usually the most useful thing on the page. This week they fell together, and the shape of the fall is the story instead.

The decision this Reading informs belongs to an allocator staring at a fast selloff in the AI chip complex and asking the obvious question: is the buildout breaking? The instrument answers more cleanly than the headline. The builders fell, but they fell less than the chips, and the market that prices a crash barely moved.

Capital

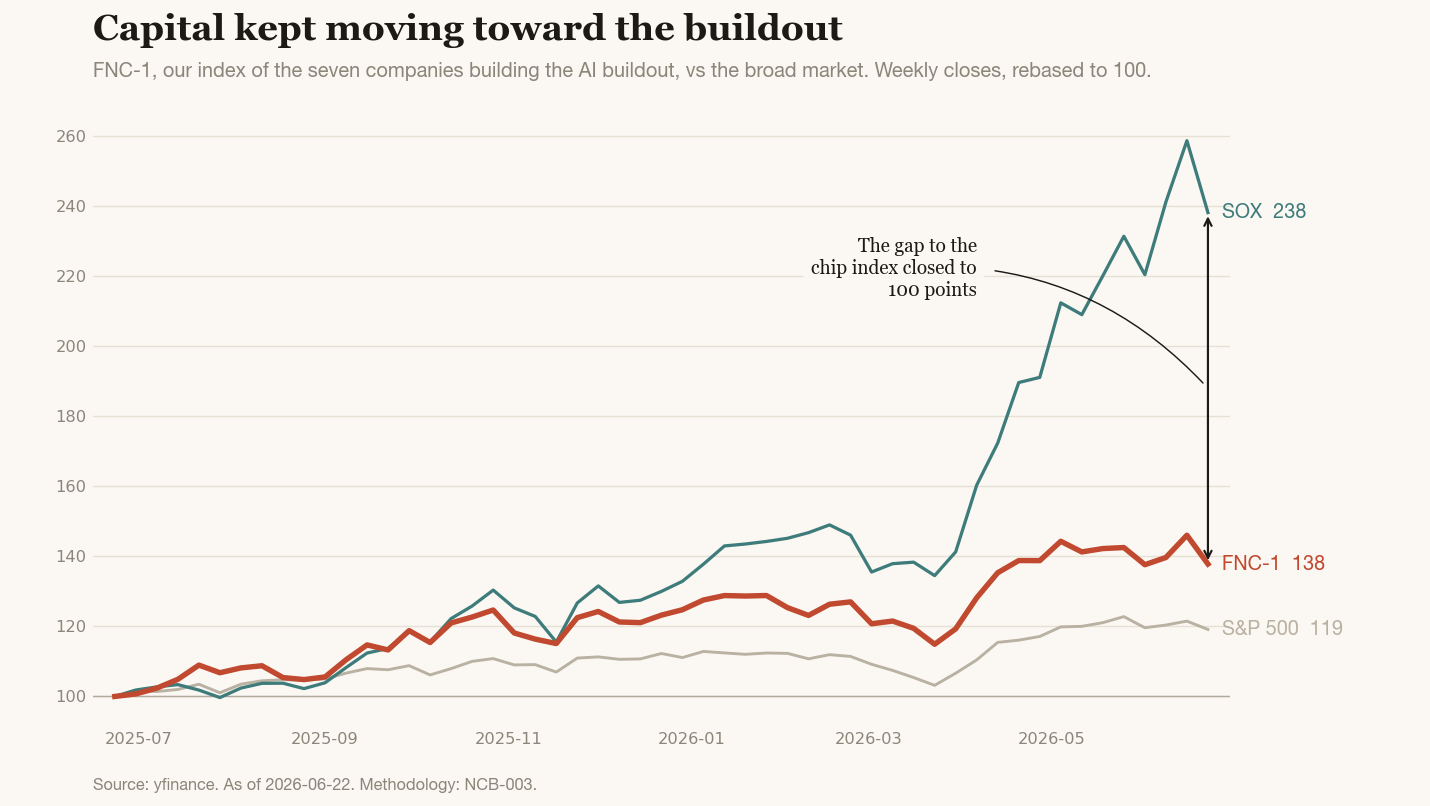

The whole complex came down this week, the chips came down hardest, and that is the only reason the gap closed. Last week the builders held while the chips sprinted and the gap widened. This week the chips gave the sprint back. The builders did the same boring thing both times: they held their relative ground while the chip index did the moving.

The binding events landed at the edge of the data window. SpaceX, which popped on its June 12 debut and ran above $200, retreated from June 17 and fell 16% on Monday, June 22, as investors questioned a valuation north of $2 trillion. The same sessions, the chip complex sold off hard: the semiconductor index dropped sharply, with Intel, Micron, and AMD each off six to eight percent, and Asia followed, South Korea's Kospi closing down 10% as SK Hynix and Samsung each fell more than 12%. The trigger was not an earnings miss. It was a repricing: scrutiny of debt-funded AI capex and a sharp hawkish turn in Fed expectations under new Chair Kevin Warsh, with traders moving to price a roughly 90% chance of a rate hike by December, up from about 57% a week earlier.

The instrument confirms the shape. FNC-1 closed the week at 137.8, up 37.8% over twelve months and down from last week's 147.3. The SOX reads 238.1, down from 261.6, a sharp one-week drop. The S&P 500 sits at 119.1, down from 124.3. All three are rebased to 100 at the start of the trailing twelve months. The gap to the SOX closed to 100 points, from 114 last week, and it closed because the chips fell about 23 points while the builders fell about 9. A gap that narrows on the chips falling is not the buildout catching up. It is the chips coming back toward a basket that never left.

The mechanism worth naming is what the SOX holds that FNC-1 leaves out: the merchant and memory names, Micron and Intel among them, the parts of the chip complex most exposed to a sentiment swing, and the parts that led this week's drop. FNC-1 holds the seven companies whose capital expenditure actually builds data centers, power, and frontier models, and they fell less because they trade on construction, not mood.

Inside the basket, the split is worth holding. Decomposed by substrate, Compute carries the index, up 74.7% on the year, while the Biological substrate is a 30% drag, down to 70. Energy sits at +42.3% and Frontier at +32.7%. The four-substrate buildout is, right now, a compute story with a biology anchor, and that concentration is the thing to watch as the cycle's leadership narrows.

Belief

The Belief Index reads 44 this week, down from 55, and below the 50 line for the first time in the series. The cooling that started last week broadened into every forward-looking bet at once.

Read

Last week the instrument showed the builders holding while the chips ran. This week it shows them holding while the chips fall. The basket sat at 147.3 then and 137.8 now, and it gave back less than the chip index did, through a week that included a 16% drop in the market's newest megacap and a double-digit rout across Asian memory names. The companies pouring the concrete came down with the tape, but they came down less than the names that trade on the speed of the story.

What the instrument shows that a single chip ticker cannot is why the gap closed. The SOX fell about 23 points and FNC-1 fell about 9. If you watched only the chip index, you would read this week as the AI trade cracking. The basket says the crack lived in the sentiment-sensitive part of the complex, the merchant and memory names FNC-1 excludes, not in the names that build. The gap closing on a chip selloff is the inverse of last week's gap widening on a chip rally, and both weeks say the chip index is the amplifier and the builder basket is the low-beta core it swings around.

Belief moved the same direction as capital this week, and the composition of the move is the tell. The Belief Index fell eleven points, and the fall came entirely from the timing bets: the OpenAI IPO odds halved again, GPT-6's release odds cooled, and the thin AGI tail thinned further. The one line that held was the crash bet. Even through the worst chip week in months, the market did not raise its odds of a bubble bursting. The crowd repriced when the acceleration arrives, not whether the floor holds.

Put the two signals together and the week has a clear shape. Capital fell but the builders fell less than the chips; belief fell but the crash odds did not rise. This is a market repricing the speed and the financing of the buildout, the debt-funded capex, the hawkish Fed, the IPO enthusiasm, without repricing its existence. That is the signature of a complex treated as long-duration construction rather than momentum. For the next two to six weeks, the gap to watch is whether the builders keep outholding the chips on the way down the way they underperformed them on the way up. A basket that falls less than the chip index in a selloff is telling you the same thing it told you in the rally: the buildout is the slow, load-bearing part, and the chips are the weather around it.

What this measures, what it does not

The Belief Index is one venue's positioning, the Polymarket panel, weighted by FP1's view of which markets matter. Individual components will be wrong, and the OpenAI IPO market may reprice again next week on a single headline. The index is a directional read on conviction, not a forecast.

FNC-1 is a measurement instrument, not an investment vehicle. It is rebased weekly to track relative movement, so the basket level matters less than the spread to the SOX. Do not read it as a portfolio.

Both fail openly. Every number here traces to the chart pipeline or a named source, every call carries a falsifier and a date, and when a read breaks we log it. The method is in NCB-003.

Cadence

The Reading runs every Monday. The next State of the Transition Briefing returns with the full correspondent desks and the Radar delta. One thread it will carry: the US–China seam moved this month, with Washington clearing advanced-chip sales that Beijing then declined, and the synthesis desk reads whether that is two systems separating or both racing for the same thing. The standing calls are tracked at fp1.ai/radar.

Methodology: NCB-003: FNC-1, the Novacene Composite.

Sources. Capital data via yfinance, weekly closes through June 22, 2026. Belief panel via Polymarket Gamma API. Semiconductor selloff, SpaceX decline, and the Kospi rout per Reuters and CNBC, June 22–23, 2026. Fed rate-hike repricing per LSEG and CME Group data cited by CBS News and Reuters, June 2026.