This Briefing tracks the structural shift from an extractive, human-bottlenecked industrial order to one organized around machine intelligence, adaptive governance, and new forms of capital allocation. The dimension this issue illuminates is duration. The Anthropocene's compute economy was built from short-lived, fungible assets financed on short horizons. The Novacene's compute economy, as of late May 2026, is being built from the longest-dated physical commitments in the cycle, leased and financed across a decade or more, wrapped around a productive core that turns over every two to three years.

Three measured facts name the question. Hyperscale tenants are now signing ten-to-fifteen-year leases, extended from the five-to-seven-year norm, with vacancy at a record 2.3% and 73% of capacity under construction pre-leased, per JLL's midyear read. High-capacity power transformers now carry lead times of up to four years, per PwC analysts cited in May, with substation units stretching from roughly 140 weeks in 2023 to above 160 in 2026, per Wood Mackenzie. And grid interconnection waits in Northern Virginia, Phoenix, and Dallas now run four to seven years, per Sightline Climate data reported by Bloomberg this month. A campus joining the Northern Virginia queue today cannot realistically draw full utility power before the early 2030s, regardless of how fast the building goes up.

The Briefing's structural read this fortnight: the cycle's commitments and its assets are priced on different clocks. The lease is the longest hand on the dial at ten to fifteen years. The power that makes the lease worth anything arrives on a four-to-eight-year delay. And the hardware that makes the power worth anything is, on the frontier, a two-to-three-year asset. Three horizons that do not nest. That gap is the cycle's second hidden balance sheet, and it is now measurable.

Radar Delta

This Briefing opens the duration-mismatch signal cluster on the Radar: five new entries that the weekly Reading will carry forward, plus one watchlist item on the principal counter-thesis.

NewTransformer and switchgear lead times as the binding delivery constraint. Substation transformer lead times have stretched from roughly 140 weeks in 2023 to above 160 weeks in 2026, per Wood Mackenzie research director Ben Boucher. PwC analysts cited in pv-magazine on May 11 put high-capacity units as long as four years; PowerMag's read of the WoodMac Q2 2025 survey placed power transformers near 128 weeks and generator step-up units near 144. Demand for step-up units rose 274% between 2019 and 2025. Roughly $2 billion of new North American transformer capacity from Hitachi Energy and Siemens Energy is projected for 2028, which does not relieve the current shortage. Switchgear sits near a year and busways have newly joined the long-lead list, per Sightline Climate. Maturity: Active. Risk: High. Next check: Wood Mackenzie Q2 2026 lead-time survey.

NewGrid interconnection queues as a multi-year gate on energization. Interconnection waits in Northern Virginia, Phoenix, and Dallas now run four to seven years, per Sightline Climate data reported by Bloomberg in May. PJM projects reaching commercial operation in 2025 averaged roughly eight years in queue. Lawrence Berkeley National Laboratory's queue research puts the national average near five years, more than double the figure of fifteen years ago. The operational consequence is that the announced pipeline is an energization curve stretching to the early 2030s, not a near-term calendar event. Behind-the-meter generation is the principal bypass. Maturity: Active. Risk: High. Next check: LBNL queue update, 2026 edition.

NewHardware useful-life and the depreciation debate. The duration mismatch in financial form. Through November and December 2025, Michael Burry argued that hyperscalers depreciating Nvidia-based hardware over five to six years against a real economic life nearer two to three were understating depreciation by roughly $176 billion across 2026 to 2028, with reported operating income at firms such as Oracle and Meta potentially overstated by more than 20%. The directional claim is corroborated by the companies themselves: Amazon shortened a subset of server useful lives from six years to five effective January 2025, citing the pace of AI development; Meta extended to five and a half; Microsoft's Satya Nadella has publicly acknowledged the obsolescence risk. Nvidia issued a rebuttal memo to analysts disputing the framing. Maturity: Active. Risk: High. Next check: hyperscaler 10-K useful-life disclosures and any further revisions.

NewLease-term extension and counterparty bifurcation. Hyperscale tenants are entering ten-to-fifteen-year-plus contracts with rent escalators, per CBRE Investment Management citing JPMorgan's December 2025 outlook, up from a five-to-seven-year norm, per JLL. Vacancy is at a record 2.3% with 8 GW under construction, 73% pre-leased; pricing has roughly doubled to $150 to $160 per kilowatt; planning timelines have expanded from 8 to 10 weeks to 18 to 24 months. The credit story is bifurcating: the four major hyperscalers carry low leverage and positive cash flow, while neocloud providers increasingly require layered credit support, including vendor and equipment-maker guarantees. The October 2025 acquisition of Aligned Data Centers for roughly $40 billion by a consortium including Microsoft and Nvidia is the cycle's first major exit precedent. Maturity: Active. Risk: Medium. Next check: CBRE and JLL year-end 2026 reports.

NewSiting resistance as a measurable cause of attrition. Community opposition has moved from background risk to a quantifiable driver of project cancellation, per Sightline Climate's May update, which has begun tracking it directly. CBRE notes rising local opposition alongside the jobs-and-tax-revenue case. The signal is that the land-and-permitting layer can strand a project independently of capital, power, or hardware. Maturity: Active. Risk: Medium. Next check: project-attrition tallies through Q3 2026.

WatchlistThe value cascade as the obsolescence counter-thesis. The bull answer to the depreciation argument is that GPUs do not fall off a cliff; they waterfall from frontier training to inference to general compute, extending economic life well past frontier life. The instrument to watch is secondary-market rental. H100 rental sits near $2.85 to $3.50 per hour, down roughly 70% from the $8 to $10 peak. The cascade is intact while the curve flattens; a drop below roughly $2.00 per hour would signal saturation rather than orderly waterfall. Maturity: Watch. Risk: Medium. Next check: H100 and Blackwell secondary pricing through Q3 2026.

Capital sub-indices

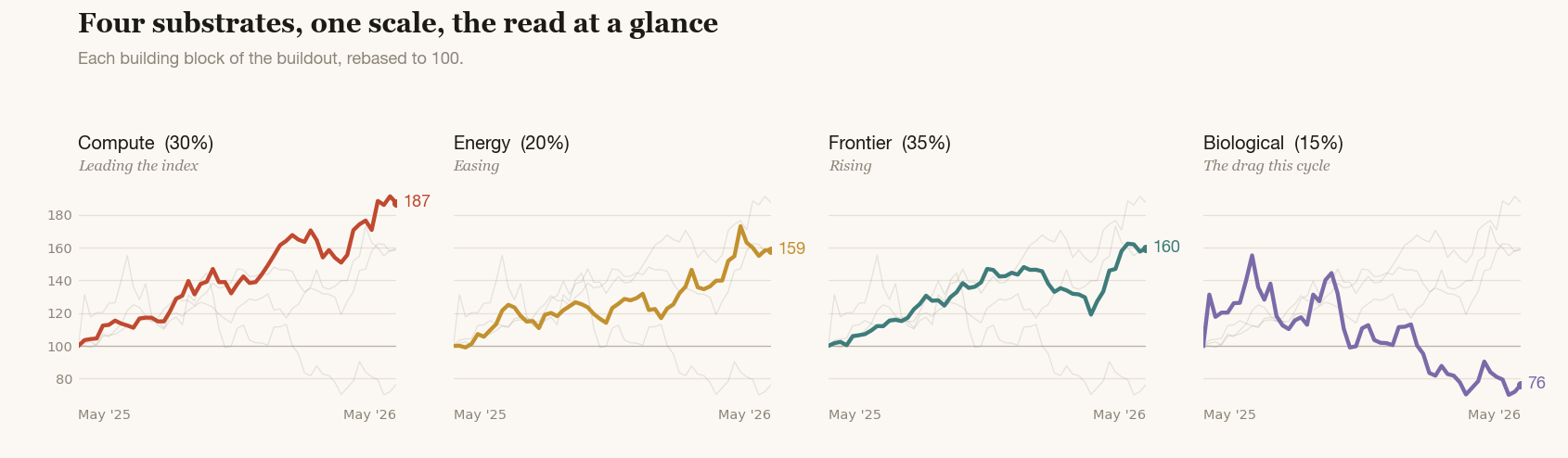

The substrate decomposition is the standing instrument of the Briefing. Two weeks past B-001, the fortnight's print is a quiet compression. Each of the three leading substrates eased; the laggard lifted; the leader-laggard spread narrowed from 127 points to 111. The composite closed at 155.2 against SOX at 265.6 and the S&P 500 at 127.1. The 110-point gap to the SOX is the period's headline read: a pure-chip cycle still well ahead of the substrate-weighted basket, with the broader composite holding above the index but trailing the semiconductor pure-play by a wide margin.

Compute (30% weight). The constituents are NVDA and ASML. The substrate closed at 187.4, +87.4% over twelve months, easing from the 194 print in B-001. The fortnight contained the May 20 NVDA fiscal Q1 release, which is now in the tape. The leader-within-leader read from R-006 and R-007, that memory has supplanted logic as the binding constraint behind the substrate's lead, is unchanged. Compute remains the index's anchor; the move this fortnight was modest.

Energy (20% weight). The constituents are CEG and GEV. The substrate closed at 158.5, +58.5%, the largest absolute pullback of the four. The PJM “Powering Reliability Through Market Design” framework introduced in B-001 remains the structural read; curtailment-first treatment for new non-capacity-backed loads continues to favor colocated baseload generation over queue-dependent power, which is the same right-of-way logic this Briefing's duration-mismatch thesis names below. CEG's structural advantage (Three Mile Island restart, Microsoft PPA inside the forward book) is intact; the fortnight's pullback is a market move, not a thesis move.

Frontier (35% weight). The constituents are MSFT and GOOGL. The substrate closed at 159.6, +59.6%, the smallest absolute pullback of the three leaders. The R-007 read that capacity-constrained Azure and TPU-monetizing GOOGL are running the same trade from opposite ends, Microsoft on enterprise distribution and Alphabet on accelerator margin, is unmoved. The substrate retains its position as the heaviest weight in FNC-1 and remains the cleanest single window onto whether the hyperscaler revenue book continues to compound faster than the substrate can deliver power.

Biological (15% weight). The constituent is RXRX. The substrate closed at 76.4, lifting from 67 in B-001 (+9.4 points over the fortnight). It is the only substrate that moved up. The structural thesis (drug discovery platforms reaching production scale, FDA AI guidance moving from draft to operational) remains directionally intact and now has a single fortnight of price action consistent with it. One fortnight is not a regime change; RXRX is a small-cap biotech and the move sits inside the range of weekly noise. The substrate stays the laggard, with the leader-laggard gap to Compute compressing from 127 points to 111. The methodology's prediction that the cycle eventually broadens into Biological is unfalsified by the fortnight and modestly better-supported, conditional on the move surviving the next two weeks.

Leader: Compute (187.4, +87.4% over twelve months). Laggard: Biological (76.4, −23.6% over twelve months). Leader-laggard spread: 111 points, compressed from 127 in B-001. Composite-to-SOX spread: −110 points (SOX leads). The composite is doing what NCB-003 said it would, surfacing where the cycle is and where it is not, with the period's read that the four substrates are moving toward each other rather than apart.

Three Horizons

Alongside the standing substrate decomposition, this issue runs a direct measurement of the mismatch the Radar Delta describes. Three horizons, three independent public sources, one gap. The decomposition above is the recurring instrument; the Horizons below are this issue's one-time lens.

Commitment (ten to fifteen years). The lease is the longest-dated element of the stack and the most contractually rigid. Record-low vacancy and 73% pre-leasing have handed pricing power to landlords, who are securing decade-plus terms with escalators against tenants who can absorb whole buildings. CBRE Investment Management notes the speculative-build risk is low precisely because the costs are high and the use cases specialized, which means the commitments are deliberate, not frothy. The exposure is not over-supply. It is the length of the promise.

Delivery (four to eight years). The lease only has value once the building draws power, and power is the slowest layer. Interconnection alone runs four to seven years in the largest markets; transformers add years on top; busways and switchgear compound it. The result is an energization curve that stretches into the early 2030s for sites entering the queue now. This is why behind-the-meter generation has become a strategic asset rather than a hedge: it is the only layer an operator can compress. Power is scarce, slow, and therefore durable.

Obsolescence (two to three years). The hardware inside the building is the shortest-lived layer and the one carrying the cycle's earnings. Nvidia's annual cadence sets a two-to-three-year frontier life; the hyperscalers' own depreciation revisions, shortening rather than lengthening, concede the direction. The open question is whether obsolescence stops at the silicon or reaches the shell. Rising rack density and the shift from air to liquid cooling mean a building designed for an earlier thermal and power envelope may not house the next generation without a retrofit whose cost is, today, under-instrumented.

The gap. The three horizons do not nest inside one another; they diverge. A ten-to-fifteen-year commitment is underwritten against power that takes half that long to arrive and hardware that turns over five to seven times across the term. The cycle's economic question follows directly: is the powered shell a durable asset whose value survives the churn of the hardware inside it, or does obsolescence cascade upward from the silicon to the building? The answer is not yet settled by evidence. It is the question the rest of this Briefing works.

Correspondent Dispatches

ConfirmedHyperscale lease terms of ten to fifteen years and longer, extended from the prior five-to-seven-year norm. CBRE Investment Management, citing JPMorgan's December 2025 outlook, and JLL's midyear research converge. Record vacancy of 2.3% and 73% pre-leasing are consistent across both desks.

ConfirmedTransformer lead times in the multi-year range. Wood Mackenzie places substation units above 160 weeks in 2026; PwC analysts cited in May put high-capacity units near four years. The figures are sourced to industry surveys rather than a single vendor, and the direction across reporting periods is consistent.

ConfirmedInterconnection waits of four to seven years in Northern Virginia, Phoenix, and Dallas. Sightline Climate data reported by Bloomberg this month, corroborated by PJM queue figures and Lawrence Berkeley National Laboratory's longer-run national average near five years.

HighThe composite delivery horizon of four to eight years from queue entry to full power. This is an assembled figure, not a single reported number, and the range is wide because it varies by market and by whether an operator pursues behind-the-meter generation. The order of magnitude is robust; the precise figure for any one site is not.

DisputedThe hardware economic life of two to three years. Michael Burry argues two to three against the hyperscalers' five-to-six-year depreciation; the value-cascade thesis argues the economic life is longer because chips waterfall from training to inference. Both are partly right, because they describe different workloads on the same asset. The contested element is the single number. The directional claim, that accounting life now exceeds frontier life, is well-supported by the companies' own revisions, including Amazon's shortening from six years to five while explicitly citing AI pace.

DisputedWhether obsolescence reaches the shell. The bull case holds power and shell as durable across hardware generations; the bear case holds that rising density and liquid-cooling requirements strand older buildings. The retrofit-cost question is genuinely under-instrumented in public data, which is itself the finding. Absence of evidence here is evidence of insufficient instrumentation, not of safety.

UnverifiedWhether any top-five hyperscaler takes a material AI-hardware write-down, or shortens useful life again, within the next four quarters. This is a forward claim. The 10-K disclosures are the place it will surface first.

Falsification candidate to watch. If interconnection or transformer lead times compress materially over the next two quarters, through queue reform biting or new transformer capacity arriving ahead of schedule, the delivery-horizon leg of the mismatch weakens and the gap narrows from the middle. That would be the cleanest single piece of evidence against this issue's thesis.

The binding constraint of the fortnight is duration. B-001 named counterparty concentration; this issue names the clock. The cycle's commitments are long-dated and rigid, the leases and the power contracts. The cycle's earnings sit in the shortest-lived layer, the hardware. The strategic act is locating where the durable value actually rests, because the lease structure is, underneath, a mechanism for allocating that duration risk between two parties.

In a powered-shell lease, the tenant owns the depreciating hardware and the landlord owns the shell and the power. Each is making a different bet. The landlord is betting that power and the building are durable, scarce, and re-leasable across hardware generations. The tenant is betting that the hardware earns back inside its two-to-three-year life. Pricing, at $150 to $160 per kilowatt with escalators, is where that risk transfer gets expressed. The question for any reader underwriting either side is which horizon they are actually long.

The positioning follows from the physics. Whoever owns power owns the durable, slow, scarce layer: interconnected sites, behind-the-meter generation, the baseload nuclear and gas-turbine assets that can serve a non-curtailable load. Whoever owns only hardware owns the fast-decaying one. The roughly $40 billion Aligned Data Centers acquisition by a Microsoft- and Nvidia-led consortium in October 2025 is the market pricing the powered shell as the durable asset. That single exit is the strongest evidence so far that the building, not the silicon, holds the duration.

Phase-transition candidate: the first visible AI-hardware write-down, or a further useful-life shortening, at a top-five hyperscaler. That event converts the depreciation debate from a research-note argument into a line in a 10-K, reprices the obsolescence horizon for the whole sector, and tests whether the cascade absorbs the churn or whether it reaches the shell.

Scenario tree, next two to four quarters.

The value cascade holds, H100 rental flattens rather than collapses, interconnection and transformer waits stay long. Then long leases on power-secured shells are rational, and the durable asset is power. The no-regret move is to commit only on sites with secured power and to push hardware-refresh risk onto the tenant. Lease timing is a function of power-securement, not the calendar.

Trigger is a stranded-shell impairment or clear evidence that rising density and liquid-cooling requirements make older buildings uneconomic to retrofit. Then lease duration on a fixed-design shell is the trap rather than the moat, and the conditional move is to shorten terms, price retrofit optionality, or refuse fixed-envelope buildings. The building's thermal design becomes the underwriting question.

Trigger is interconnection reform biting or transformer capacity arriving ahead of the 2028 schedule. Then the scarcity premium on power erodes, the durable-asset thesis weakens from the middle, and the four-to-eight-year delivery horizon, the load-bearing leg of the mismatch, shortens. Pricing softens as supply catches the queue.

Trigger is the frontier-maturation read carrying through: if model differentiation moves to cost and distribution and capex discipline arrives, lease demand softens. Then 73% pre-leasing and record pricing read as a top rather than a floor, and the counterparty-concentration risk from B-001 converges with the duration risk here into a single repricing.

Adversarial read of FP1's working thesis. This Briefing treats the duration mismatch as a fragility to be measured. The strongest counter is that the mismatch is the business model, not the bug. The powered shell is deliberately engineered as a long-lived, utility-like asset, and the fast hardware churn inside it is the tenant's problem by design, not the asset's. If that is right, the mismatch is a risk-transfer mechanism that concentrates durable value in whoever owns power, and FP1's framing risks mistaking an allocation of risk for a systemic fault. The test is empirical and singular: does the powered shell hold value across a full hardware generation? The Aligned exit says yes so far. A stranded-shell write-down would say no.

The parallel that fits this fortnight is not the bubble that everyone reaches for. It is the infrastructure that came just before the one that mattered. Consider the canals.

Britain's canal network, built across the late eighteenth and early nineteenth centuries, was the dominant freight infrastructure of its age. It drew enormous speculative capital in the canal mania of the 1790s. It was fixed, immobile, and financed against payback horizons measured in decades. The demand it served was real and growing. And within roughly a generation, a faster-moving substrate, the railway, rendered much of it economically obsolete. Canal companies' physical assets stranded; many were bought out by the railways that had superseded them. The builders did not fail to see that freight demand was real. They failed to ask whether their fixed asset's payback horizon was shorter than the arrival of the next technology.

The mechanics apply directly. A hyperscale building is committed, leased and financed, for ten to fifteen years, against a productive core that turns over every two to three. Demand for compute is real and growing, exactly as freight demand was. That is not the question. The question is whether the durable asset's horizon outruns the cycle that will supersede what runs on top of it.

But the canal teaches a second lesson, sharper than the first. Not all of the canal stranded. The right-of-way, the land, the grading, the cuttings, sometimes carried the railway that replaced the water. The locks and the barges did not. In every duration mismatch there is a layer that is the right-of-way, durable and re-usable across the cycle, and a layer that is the water, specific and fast-obsoleting. Here the right-of-way is power and interconnection, the scarce and slow layer that holds value across hardware generations. The water is the hardware, and possibly the thermal and power-density design of the shell that houses it. Which one the building is, right-of-way or water, is the whole question.

The first-principles imperative for the institutional reader paid to be right about the Transition: when underwriting a long-dated data-center commitment, separate the right-of-way from the water before you separate anything else. Power access and interconnection are the right-of-way; they survive the churn. The thermal envelope of the shell is the open case. If the building cannot be re-fitted for the next generation's density, you have not leased a railway bed. You have leased a canal, and the water is already running out of it.

Implications

The lease outlives the asset inside it. That is the cycle's second underwriting question. B-001 named counterparty concentration: who is on the other side of the long-dated revenue book. B-002 names duration: how long the commitment outlasts the productive asset. The two compound. The cycle is building decade-plus commitments to two-to-three-year assets, underwritten by a small set of counterparties whose own forward spend already exceeds their current revenue. Concentration and duration are the same balance sheet read from two angles.

Power is the right-of-way. Own it or secure it. The durable, scarce, long-lived layer of the stack is power and interconnection, not silicon and not, by itself, the building. The roughly $40 billion Aligned exit priced this directly. The practical consequence is that a lease-timing decision is, underneath, a power-securement decision: a contract on a power-secured site is a fundamentally different asset from one dependent on a four-to-seven-year queue, even at the same headline term and price.

Lease timing is a power-and-design question, not a market-timing one. For the reader facing a commit-or-wait decision, the useful question is not whether the market is near a top. It is whether this specific site's power is durable and whether this specific shell can be re-fitted for the next density generation. Commit on power-secured, design-flexible sites; wait, shorten, or price in optionality where either is in doubt. The calendar is the wrong instrument. The site's two horizons, power and thermal envelope, are the right ones.

The depreciation disclosures are the canary. The single highest-information event over the next four quarters is the 10-K. The first top-five hyperscaler to shorten AI-hardware useful life again, or to book a related write-down, converts the obsolescence horizon from a contested two-to-three-year estimate into a reported number, and reprices every long-dated commitment underwritten against the longer assumption. Watch the filings before the equity research.

Cadence

The standing Radar now sits with the weekly Reading. The next Capital and Belief Reading runs Monday, June 1 (R-010), and will begin carrying the five duration-cluster signals opened here. The next Briefing runs Thursday, June 11 (B-003), with the first revisions to this issue's scenario tree, gated on the 10-K depreciation disclosures and the next interconnection and transformer reads.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through May 25, 2026

- CBRE Investment Management, “Data Centers: Ain't No Mountain High Enough” (lease terms 10–15+ yr citing JPMorgan, Dec 2025; Aligned exit)

- JLL, “Data center market defies early 2025 turbulence”, Oct 14, 2025 (vacancy 2.3%, 73% pre-leased, pricing, lease and planning timelines)

- Data Center Frontier, “Two Lenses on One Market: JLL and CBRE”, Aug 27, 2025

- Data Center Knowledge / Wood Mackenzie, “AI Data Center Boom Rewires US Power Supply Chain” (transformer 140→160+ wk; interconnection; market sizing)

- pv magazine USA, “U.S. transformer market faces severe supply constraints”, May 11, 2026 (PwC four-year lead times; +274% GSU demand)

- POWER Magazine, “Transformers in 2026”, Jan 2, 2026 (WoodMac Q2 2025: power transformers ~128 wk, GSUs ~144 wk)

- Sightline Climate data reported by Bloomberg, May 2026 (interconnection 4–7 yr in Northern Virginia, Phoenix, Dallas; busways and battery backup as new long-lead items; siting attrition)

- Lawrence Berkeley National Laboratory, queue research (“Queued Up” series): national interconnection average near five years, more than doubled over fifteen years

- CNBC, “How long before a GPU depreciates?”, Nov 14, 2025 (Burry 2–3 yr useful-life argument; Nvidia rebuttal)

- Levelheaded Investing, “Are AI Chips' Useful Lives Creating Useless Earnings?”, Dec 2025 (~$176B understated depreciation 2026–28; >20% profit overstatement at Oracle/Meta, per Burry)

- Stanley Laman Group, “Why GPU Useful Life Is the Most Misunderstood Variable”, Nov 21, 2025 (Nvidia annual cadence; Nadella obsolescence comment; H100 rental $2.85–3.50/hr)

- Amazon FY2024 and FY2025 Form 10-K, server useful-life disclosures (shortened six years to five effective Jan 1, 2025, citing AI/ML pace); Meta useful-life extension to 5.5 years

- State of the Transition Briefing B-001

The lease is the longest hand on the dial.

The power arrives on a delay.

The asset inside is already obsolescing.

The Briefing tracks the system. The Radar holds the threads.