This Briefing tracks the structural shift from an extractive, human-bottlenecked industrial order to one organized around machine intelligence, adaptive governance, and new forms of capital allocation. The dimension this issue illuminates is the cycle's underwriting question. The Anthropocene's compute economy was built on diffuse consumer demand and many counterparties. The Novacene's compute economy, as of mid-May 2026, is built on concentrated revenue commitments from a handful of frontier labs against physical infrastructure constraints that the substrates cannot quickly fix.

Three events in eight days named the question. On May 7 the European Council and Parliament agreed on the Digital Omnibus, deferring high-risk AI obligations from August 2026 to December 2027 for standalone systems and August 2028 for embedded systems. On May 8 the Financial Times reported Anthropic in advanced talks at a near $1 trillion valuation against $45 billion of annualized revenue, a fivefold print in eighteen months. On May 14 Cerebras Systems priced its IPO at $185 and closed up 68% at $311.07 on a fully diluted valuation near $95 billion, the largest US tech IPO since Uber in 2019, with demand twenty times oversubscribed. Two of the three are confirmations of acceleration. The third is the question that follows from them.

The Briefing's structural read this fortnight: capex is no longer the binding question. Counterparty concentration is. Cloud-provider revenue backlog now stands near $2.1 trillion across Amazon, Google, Microsoft, and Oracle, and roughly half of that sits with two cash-burning labs. That is the cycle's hidden balance sheet.

Radar Delta

This is the first Briefing under the new cadence, so the Radar Delta opens with three new entries, two reframings, one falsification, and one watchlist update.

NewHBM as the binding constraint inside Compute. R-006 named the substrate ranking change. R-007 confirmed it as a physical limit. The Briefing places it on the Radar formally. Goldman Sachs raised its 2026 DRAM supply-demand gap forecast from 3.3% to 4.9% in April, the most severe shortage in fifteen years. SK Hynix and Micron capacity sold out through 2026; Samsung's Kim Jaejune warned of “significant shortages” through at least 2027 in the company's April 30 earnings release. Reuters reported on May 8 that tech firms have offered to fund SK Hynix lithography purchases to secure allocation. Maturity: Active. Risk: High. Next check: NVDA earnings May 20, where memory cost commentary will be the read inside the headline number.

NewPJM large-load curtailment moves to FERC filing track. PJM Interconnection released “Powering Reliability Through Market Design” on May 6, naming the transition from “an era of managing surplus to an era of managing scarcity.” Member proposal target is a FERC filing by year-end, with the framework operational by the 2028/2029 capacity auction in June 2026. Loads of 50 MW or more at a single point of interconnection are now subject to curtailment-first treatment during reliability events under the non-capacity-backed-load structure. The proposal does not cap data-center growth; it conditions interconnection on either bringing new generation or accepting earlier curtailment. Maturity: Active. Risk: Medium. Next check: FERC filing Q4 2026.

NewAI infrastructure IPO window opens. Cerebras Systems priced May 13 at $185, well above its raised $150 to $160 range. The 30-million-share offering raised $5.55 billion, the largest US tech IPO since 2019. Demand was reported by Bloomberg at twenty times available shares. CEO Andrew Feldman told CNBC that customer concentration remains the structural risk: 86% of 2025 revenue came from two UAE-linked customers, primarily G42 and the Mohamed bin Zayed University of Artificial Intelligence. The signal is not the chip story. The signal is that the public-market window for AI infrastructure has opened. Maturity: Active. Risk: Medium. Next check: lock-up expiry and Q2 results.

ResolvedEU Digital Omnibus deadline shift. Falsification of the open thread from Issue 001. The trilogue at 4:30 a.m. on May 7 produced a provisional political agreement. Standalone high-risk AI systems under Annex III now have until December 2, 2027 to comply. Embedded systems under Annex I have until August 2, 2028. Watermarking obligations under Article 50(2) move to December 2, 2026, three months past the original date. The deal also introduces an EU-wide ban on AI systems whose primary purpose is to generate non-consensual intimate imagery. Formal adoption is expected between June and July, before the original August 2 deadline. The thread opened in Issue 001 (March 30) is closed. The compliance horizon for European AI deployment has moved by sixteen months.

ReframedHyperscaler debt-to-revenue ratio recast as counterparty concentration. The Issue 001 thread placed this on the Radar as a capital-structure risk. The cleaner instrument as of this fortnight is counterparty concentration. The Information reported on May 5 that Anthropic agreed to pay Google roughly $200 billion over five years for 5 gigawatts of TPU capacity. CNBC confirmed on May 6 that Anthropic took the entire Colossus 1 capacity at SpaceX in Memphis, plus stated interest in multi-gigawatt space-based compute. Engadget summarized the resulting cloud-provider backlog at approximately $2 trillion across Amazon, Google, Microsoft, and Oracle, with OpenAI and Anthropic commitments accounting for the majority. The financial structure being built is unusual. Two counterparties at negative free cash flow are now responsible for roughly half of the long-dated revenue book at four publicly traded hyperscalers. Maturity: Active. Risk: High.

HardenedFrontier revenue verification. Anthropic's annualized revenue at $45 billion against $9 billion at end-2024, per FT and corroborated by The Information, is a fivefold print in eighteen months. Reported gross margin near 70%, up from 38%, against $30 billion in February. The structural revenue thesis has moved from claim to evidence. The question of whether AI lab revenue is real has been answered. The question of whether it is sufficient to underwrite the cycle has not. Maturity: Maturing. Risk: Medium.

WatchlistNVDA fiscal Q1 print, May 20. Consensus revenue near $78.8 billion with EPS at $1.77 against company guide of $78 billion plus or minus 2%. Goldman Sachs at $80.8 billion. Polymarket implied probability of beat near 90%. The Briefing's interest is in the substrate-ranking detail rather than the headline: how much of the print is attributable to memory cost pass-through, what the gross margin commentary looks like against R-006's HBM observation, and whether the Q2 guide names energy or memory as the binding constraint on capacity.

Capital sub-indices

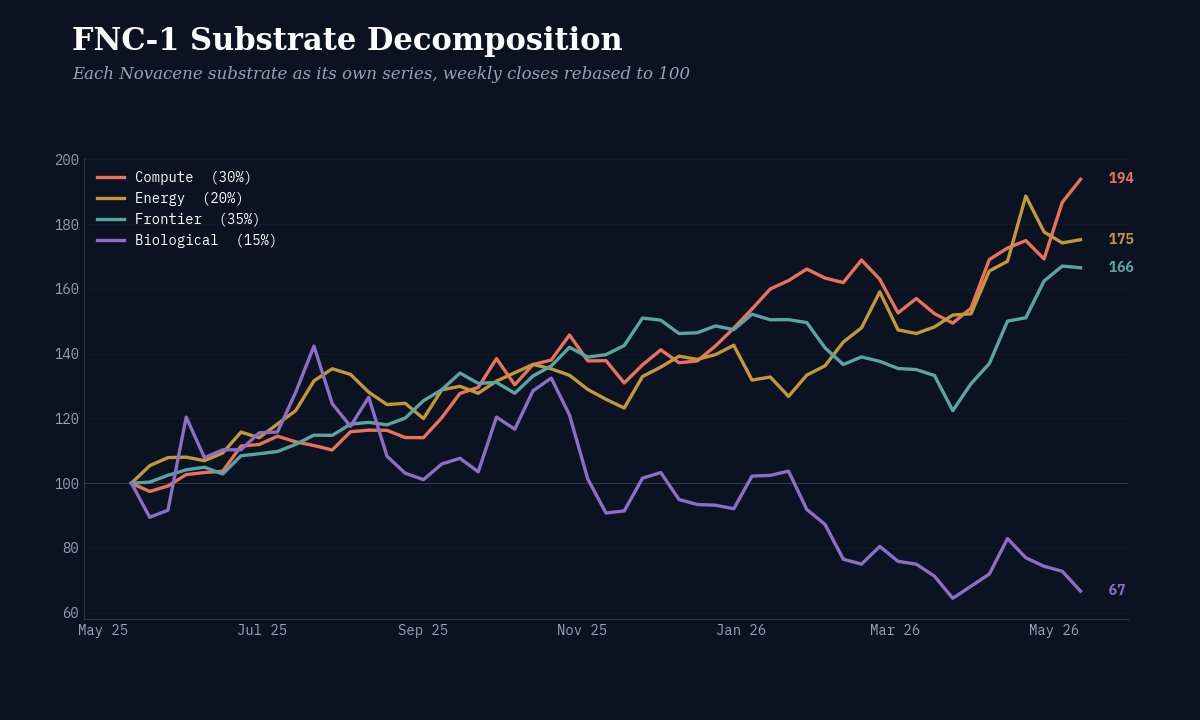

The substrate decomposition runs every Briefing from B-001. Where R-006 and R-007 reported the FNC-1 composite against the SOX, the Briefing decomposes the basket by Novacene substrate. The leader-laggard spread, and the substrate doing the heavy lifting, is the read.

Compute (30% weight). The constituents are NVDA and ASML. The substrate is moving on two distinct mechanics. NVDA gave back 8.4% from the April 27 high in the first half of R-006's window and recovered through Friday May 8, closing at $215.20. ASML continues to track the broader semiconductor capex cycle. The leader-laggard within the substrate is now memory rather than logic. HBM capacity sold out through 2026 across all three suppliers reframes the substrate. Compute as measured by NVDA + ASML is leading the composite. Compute as measured by memory is the binding constraint behind the lead.

Energy (20% weight). The constituents are CEG and GEV. The substrate's bull thesis through Q1 was the nuclear PPA cluster and the GE Vernova turbine cycle. The PJM May 6 memo introduces a second-order question: if grid power becomes the curtailment-first interconnection class for new data centers, the economic value of a colocated baseload generation asset rises relative to a queue-dependent one. CEG, with the Three Mile Island restart and Microsoft PPA already inside its forward book, is structurally insulated. GEV's order book skew toward gas turbines for behind-the-meter colocation is the question. The substrate ranking inside Energy is shifting toward generation that can credibly serve a non-curtailable load.

Frontier (35% weight). The constituents are MSFT and GOOGL. The substrate is the heaviest weight in FNC-1 and the substrate that absorbed the largest period news. Alphabet's stock closed up roughly 1.5% on the day The Information reported the $200 billion Anthropic commitment, holding gains through the week. Per Kalshi, Alphabet's odds of finishing 2026 as the world's largest company by market value moved from 23.5% to 29.5% between May 7 and May 11. Microsoft's Azure capacity-constrained commentary from R-006's earnings call clusters with the Anthropic capacity strain into a coherent read: the hyperscaler revenue book is filling faster than the substrate can deliver power, memory, or training cycles. The Frontier substrate is leading on backlog. It is constrained on delivery.

Biological (15% weight). The constituent is RXRX. The substrate has been the FNC-1 drag through the inaugural quarter and remains so. No period catalyst. The structural thesis, drug discovery platforms reaching production scale and FDA AI guidance moving from draft to operational, is intact but unmoved this fortnight. The substrate ranking inside FNC-1 is unchanged: Biological is the laggard, and the gap is the cleanest indicator that the AI transition is not yet broadening into the substrate the methodology says it eventually must.

Leader: Compute (194, +93.8% over twelve months). Laggard: Biological (67, -33.3% over twelve months). Leader-laggard spread: 127 points. The composite is doing what NCB-003 said it would, surfacing where the cycle is and where it is not.

Correspondent Dispatches

ConfirmedAnthropic's annualized revenue at approximately $45 billion. The Financial Times, Bloomberg, and The Information independently report the number from sources inside the funding-round discussions. The figure is consistent with the $30 billion February data point and CFO Krishna Rao's reported timeline.

ConfirmedThe EU Digital Omnibus political agreement on May 7. The European Council, the European Parliament, and the European Commission have published consistent accounts. Standalone Annex III high-risk obligations move to December 2, 2027. Embedded Annex I obligations move to August 2, 2028. The thread from Issue 001 is closed at this confidence level.

ConfirmedThe Cerebras IPO outcome. Pricing at $185, the $5.55 billion raise, the close at $311.07 on May 14, the 68% day-one return. CNBC, Bloomberg, Yahoo Finance, and the Wall Street Journal converge on the same numbers.

HighCloud-provider revenue backlog near $2 trillion across Amazon, Google, Microsoft, and Oracle. The number is assembled from public Q1 disclosures and reporting from The Information and Engadget. Approximately half of the long-dated component is attributable to OpenAI and Anthropic commitments. The aggregation methodology varies across sources; the order of magnitude is settled.

DisputedAnthropic's reported gross margin near 70%, up from 38%. This is sourced to people familiar with the company and has not been published in audited financials. The implication, if confirmed, is that inference cost per unit has dropped materially or that pricing power is firmer than R-006 modeled. Treat as a sourced claim, not a financial fact.

DisputedThe $1 trillion valuation headline. The actual reporting points to talks at up to $50 billion in primary against pre-money near $900 billion. The headline number depends on the close. No term sheet has been signed.

UnverifiedWhether the Anthropic round closes inside two months. The FT framing is a target, not a commitment.

FalsifiedThe Issue 001 base-case assumption that the EU high-risk obligations would activate August 2, 2026 absent a formal Omnibus adoption. The trilogue closed on May 7, and formal adoption is on a June-July timeline.

Falsification candidate to watch. If the May 20 NVDA print materially under-clears the Visible Alpha consensus on either revenue or gross margin, the substrate-leadership read of the last three Readings comes into question. The R-007 hypothesis (capital broadening within the chip complex faster than the diversified basket can absorb) is the active claim. A miss would falsify it.

The binding constraint of the fortnight is no longer capacity. It is concentration. Capex is confirmed at the high end. Memory and power are physical constraints with multi-year resolution paths. What changed in fourteen days is the visibility into who is on the other side of the trade.

Cloud-provider revenue backlogs are public information. The Information's estimate places the cloud-provider AI-related backlog near $2 trillion, with OpenAI and Anthropic collectively representing roughly half of the long-dated component. Both labs are still at negative free cash flow at corporate level. Anthropic's contracted forward spend on Google Cloud alone, at approximately $40 billion per year beginning 2027, exceeds its current annualized revenue. The structure works only if the revenue compounds.

Three actors are moving and the incentives are now legible. Alphabet is monetizing TPU capacity at scale, with Google Cloud operating margin reportedly tripling from 9.4% in Q1 2025 to 32.9% in Q1 2026. Microsoft is monetizing the inverse asymmetry, with Azure capacity-constrained through year-end and $190 billion of FY26 capex committed. SpaceX is positioning Colossus and Terrafab as the alternative cloud, with Anthropic now the anchor tenant for both Colossus 1 and the proposed multi-gigawatt space-based capacity. The three are competing on different binding constraints. Alphabet on TPU performance. Microsoft on enterprise distribution. SpaceX on physical buildout speed.

Phase-transition candidate: the moment Alphabet's market cap crosses Nvidia's. The spread closed at roughly $400 billion as of Friday May 8 with NVDA at $5.2 trillion and GOOGL at $4.8 trillion. Kalshi prices Alphabet ending 2026 as the largest company at 29.5%. The mechanism is straightforward. If the Anthropic backlog and the TPU monetization story drive the next Q2 Alphabet print materially above consensus, the spread compresses. The NVDA May 20 print is the symmetric event. The phase transition is not whether either company is up. It is which one absorbs the next dollar of incremental AI revenue capture inside the substrate.

Scenario tree, next six to twelve weeks.

The cycle continues at its current shape. FNC-1 to SOX spread holds near 90 points. Belief Index stabilizes in the 48 to 55 corridor. Substrate ranking unchanged: Compute leading, Energy second, Frontier on backlog, Biological dragging.

Trigger is gross margin commentary citing memory cost pass-through inside the FY27 guide. If: SOX corrects, FNC-1 to SOX spread compresses, Compute substrate decomposes between logic (NVDA, ASML) and memory (not in current FNC-1 constituent list, which is a methodology gap NCB-003 will need to address in v0.2). Bubble-burst component on the Belief Index moves further; the 9-point move on May 11 may be the first leg, not the last.

Trigger is a term sheet at the high end inside the next four weeks. If: the private-market AI ceiling resets, secondary-market AI exposure repricing forces fund NAV adjustments, and the counterparty-concentration question moves from research note to credit-committee question. The Bank of England flag from R-007 becomes a leading rather than concurrent indicator.

Trigger is a Q3 filing rather than Q4. If: data-center colocation economics change quickly, Constellation Energy and Vistra repricing accelerate, and the Energy substrate inside FNC-1 takes leadership from Compute for the first time since the inaugural reading.

Adversarial read of FP1's working thesis. The State of the Transition framing treats the AI transition as a substrate-broadening process where Compute is leading and the other three substrates eventually catch up. The fortnight's evidence supports a different read. The cycle may not broaden. It may concentrate further. Two labs, two clouds, one chipmaker, and a small set of power and memory suppliers may capture the bulk of the rents for the next several years. If concentration is the destination rather than a phase, then the FNC-1 methodology may need to weight the cycle's concentration risk explicitly rather than treating it as a diversification benefit.

Consider the cycle from a distance. A handful of laboratories are building intelligence at a scale that requires the largest single capital commitments in private-market history. They are funded by hyperscalers who are themselves funded by debt and by the same labs' compute commitments. The structure is reflexive. Capital flows from Alphabet into Anthropic, and from Anthropic back into Alphabet, multiplied. The parallel that suggests itself is not the railroad cycle, though that one will be invoked frequently this quarter. The parallel is the medieval banking houses.

The Medici, the Fugger, and the houses of Florence and Augsburg in the fifteenth and sixteenth centuries operated as both lender and depositor inside a small concentrated network. They financed sovereign borrowers whose ability to repay depended on the houses' continued willingness to refinance. The structure produced extraordinary returns when the cycle held and catastrophic losses when a single counterparty failed. The Fugger collapse in the 1570s was not caused by an external shock. It was caused by the Habsburg crown defaulting on debts the Fugger had no realistic way to diversify away from.

The mechanics apply here. The hyperscaler revenue book is concentrated on two cash-burning counterparties whose ability to pay the contracted compute spend depends on the same capital markets that fund the hyperscalers' debt issuance. The structure is profitable as long as revenue compounds and capital remains available. It is fragile in exactly the way the Augsburg banking houses were fragile.

What did the Fugger fail to see? They believed their counterparty was the Habsburg state, which could not fail. The counterparty turned out to be the Habsburg cash flow, which could and did. The lesson for the present moment is identical. The hyperscalers believe their counterparty is the existence of OpenAI and Anthropic as going concerns. The actual counterparty is the labs' revenue trajectory. Going concern is necessary but not sufficient.

The deeper transition this fortnight reveals is the move from Anthropocene compute economics to Novacene compute economics. The Anthropocene's compute economy was paid for by hundreds of millions of consumer subscriptions and millions of enterprise seats. Counterparty risk was diffuse by construction. The Novacene's compute economy is paid for, increasingly, by a structurally small number of frontier-lab principals whose forward revenue commitments dwarf the consumer base in dollar terms. The economic substrate of compute is shifting from many small counterparties to a few enormous ones. That is a different kind of economy.

The first-principles imperative for the institutional reader paid to be right about the Transition: revisit the counterparty mapping in the AI exposure book. If the answer to “what is the counterparty on this position” terminates in “Alphabet” or “Microsoft” but the underlying revenue stream terminates in “Anthropic” or “OpenAI,” then the position is exposed to lab credit and lab capital availability, not hyperscaler credit. Most existing risk frameworks are not pricing that exposure. They will need to.

Implications

The capex thesis is settled. The counterparty thesis is the open question. The R-006 and R-007 evidence closes the structural question of whether the cycle is real and at what scale. Combined hyperscaler 2026 capex above $700 billion, Anthropic revenue at $45 billion annualized, Cerebras pricing twenty times oversubscribed. The next phase of FP1's instrumentation needs to address what underwrites the cycle. The cloud-provider backlog and its counterparty concentration are now the leading indicator. We expect this to surface in credit research before it surfaces in equity research.

The Compute substrate inside FNC-1 needs a memory representative. The v0.1 methodology constituents are NVDA and ASML. The fortnight confirmed that the binding constraint inside Compute is HBM rather than logic. SK Hynix is not a US-listed equity and is not in the current basket. NCB-003 v0.2 will need to address whether the substrate's measurement instrument carries the constraint that defines the substrate's behavior. Until then, the FNC-1 to SOX spread, where the SOX has indirect memory exposure through KLAC, AMAT, and LRCX, is a more complete instrument than FNC-1 alone for tracking the period's binding constraint.

The EU governance horizon has cleared, and that fact is itself the story. Issue 001 placed the EU Digital Omnibus deadline shift on the Radar at Medium risk. The May 7 trilogue resolves it. The horizon for European compliance has moved from August 2026 to December 2027 for standalone systems and August 2028 for embedded systems. The cleared horizon removes a meaningful overhang on European AI procurement. We expect frozen procurement budgets to begin releasing through Q3 2026. The structural read: the bottleneck on AI deployment in Europe was not capability or capital. It was certainty. The certainty has arrived.

Cadence

The next Capital and Belief Reading runs Monday, May 18 (R-008). The next Briefing runs Thursday, May 28 (B-002), with the second substrate sub-index decomposition and the first scenario revisions from this Briefing's tree.

Full watchlist at fp1.ai/radar.

Sources

- yfinance / public market data, weekly closes through May 8, 2026

- Financial Times, “Anthropic weighs deal for near $1tn valuation as revenue surges”, May 8, 2026

- Bloomberg, Anthropic funding-round reporting, May 7–12, 2026

- The Information, “Anthropic Commits to Spending $200 Billion on Google's Cloud and Chips”, May 5, 2026

- CNBC, “Anthropic, SpaceX announce compute deal that includes space development”, May 6, 2026

- PJM Interconnection, “Powering Reliability Through Market Design”, May 6, 2026

- Council of the EU, “Council and Parliament agree to simplify and streamline rules on AI”, May 7, 2026

- Hogan Lovells, “EU legislators agree to delay for high-risk AI rules”, May 7, 2026

- CNBC, “Cerebras pops 68% in Nasdaq debut, pushing AI chipmaker's market cap to $95 billion”, May 14, 2026

- Fortune, “Cerebras stock surges in Nasdaq debut after blockbuster AI IPO”, May 14, 2026

- Reuters, “SK Hynix offered customer-funded production lines”, May 8, 2026

- Tom's Hardware, Samsung and SK Hynix memory shortage warning, April 30, 2026

- Goldman Sachs, “2026 DRAM Supply-Demand Forecast,” April 2026

- NVIDIA Corporation fiscal 2027 Q1 earnings preview; consensus data via Visible Alpha, May 11, 2026

- Polymarket — NVDA beat expectations Q1 FY27

- State of the Transition Reading R-006 and Reading R-007

Capex was confirmed.

Then the cycle named its counterparties.

The question moves from scale to underwriting.

The Briefing tracks the system. The Radar holds the threads.