I. Opening Analysis: The Tariff Fulcrum

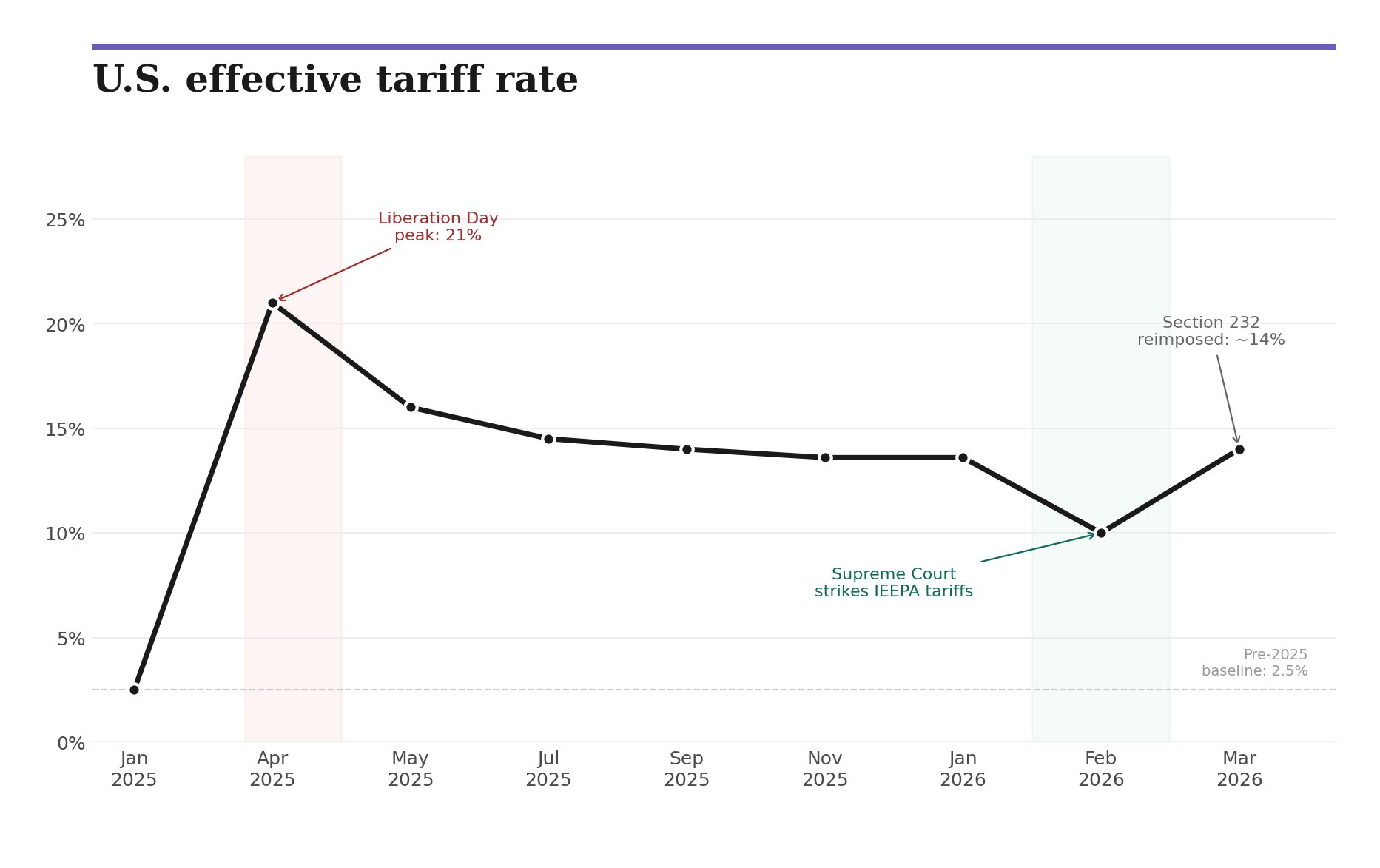

One year ago this week, the President declared Liberation Day. In the twelve months that followed, U.S. trade policy changed more than 50 times. The effective tariff rate peaked at 21%, fell to 13.6% by year-end 2025, and was further reduced after the Supreme Court struck down the IEEPA-based tariffs in February 2026. The current effective rate sits around 14%.

For the AI infrastructure buildout, the tariff episode has produced three lasting effects:

1. Planning horizon compression. Hyperscalers that once planned GPU procurement 18-24 months ahead shortened that window to 6-9 months during the tariff volatility. Capital allocation decisions worth tens of billions were made under radically uncertain cost assumptions. Some of those decisions, particularly around data center site selection and chip sourcing, are now locked in and cannot be reversed.

2. Supply chain diversification as a permanent cost. The tariff episode accelerated efforts to reduce dependence on single-source chip supply chains. Cerebras on AWS, Google's TPU expansion, and Amazon's Trainium chips are all partly responses to the risk that tariffs could raise the cost of Nvidia GPUs by 25% overnight. This diversification adds engineering complexity and cost but reduces concentration risk.

3. The Section 232 overhang. The broadest tariffs were struck down, but semiconductor-specific tariffs remain active. A 25% duty applies to specific AI accelerators (H200, MI325X) destined for re-export. Commerce is required to deliver a semiconductor market report to the President by July 1, 2026, with authority to recommend further tariffs. CSIS estimates current and proposed tariff policies threaten $75-100 billion in additional AI infrastructure costs over five years, equivalent to 15-20 fewer hyperscale facilities.

The AI buildout did not pause during this period. Combined hyperscaler capex for 2026 is projected at $660-690 billion. But the buildout is now priced to include tariff risk as a permanent variable, not a transient shock.

II. Signal Analysis

Signal 1: OpenAI's $122 Billion Round

OpenAI closed the largest private financing in history: $122 billion at an $852 billion post-money valuation. The investor composition reveals the nature of the bet:

- Amazon: $50 billion (starting with $15 billion upfront, $35 billion conditional on milestones)

- Nvidia: $30 billion (largely in dedicated GPU capacity commitments, not cash)

- SoftBank: $30 billion (three $10 billion tranches: January, April 1, July)

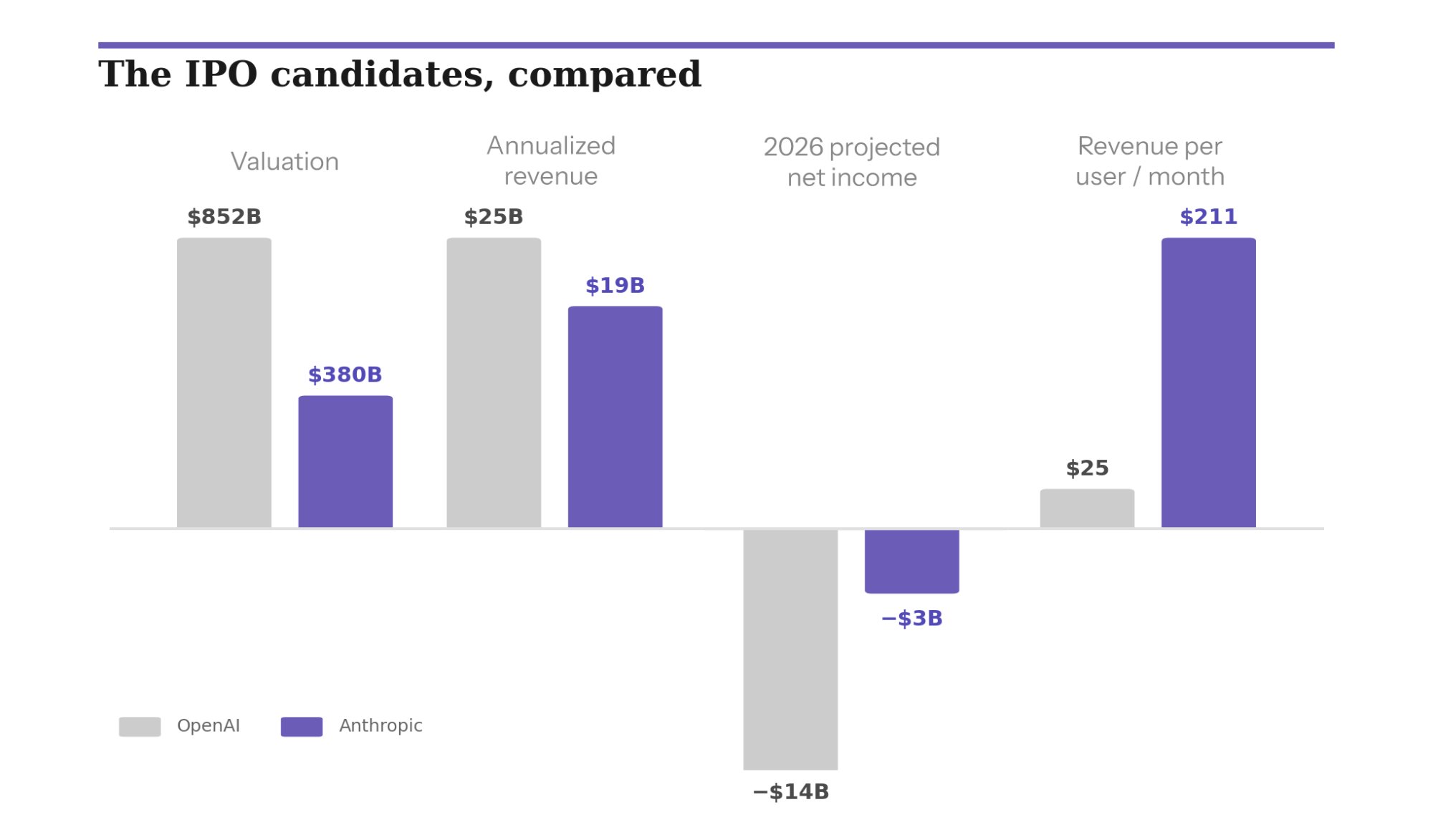

This is not venture capital in any traditional sense. It is industrial policy conducted through private balance sheets. OpenAI projects $25 billion in annualized revenue for 2026 but losses of approximately $14 billion. Projected cumulative spending through 2029 totals $115 billion.

The valuation implies 34x forward revenue on a company with negative margins. For comparison, Salesforce at its peak traded at approximately 15x forward revenue with positive operating margins. The market is pricing OpenAI not as a software company but as a platform that will capture a share of global enterprise software spending. Whether that thesis is correct depends on whether consumer-subsidized engagement metrics convert to enterprise revenue at scale.

Signal 2: Anthropic's Enterprise Inversion

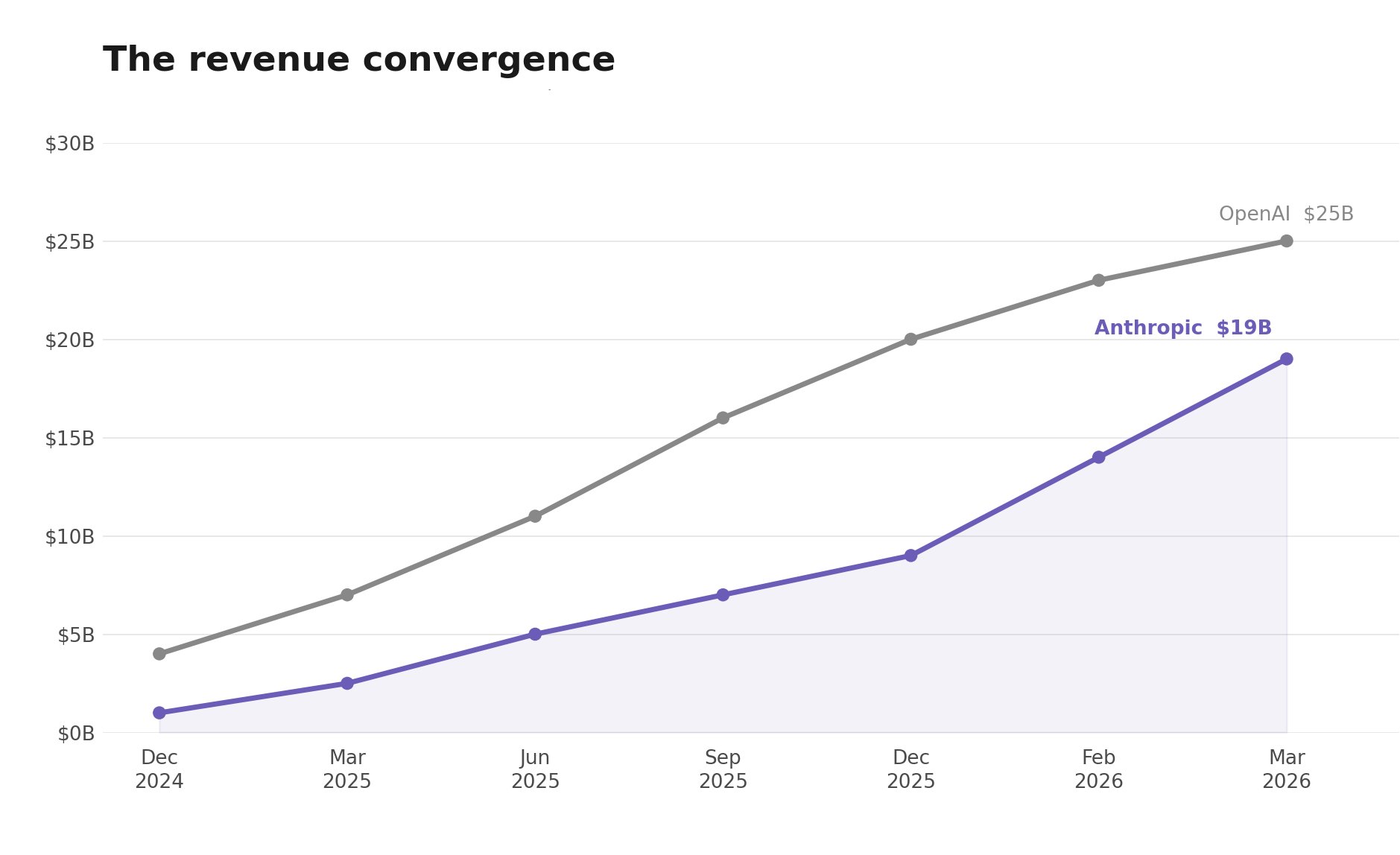

The enterprise AI spending data has shifted materially. According to Ramp Economics Lab, Anthropic's share of combined OpenAI-plus-Anthropic enterprise spend has moved from roughly 10% at the start of 2025 to over 65% by February 2026. Ten weeks ago, the split was 50/50. It is now approximately 60/40 in Anthropic's favor.

The drivers are structural:

- Claude Code now generates $2.5 billion in annualized revenue, having more than doubled since the start of 2026. It is responsible for 4% of all public GitHub commits, with projections of 20%+ by year-end 2026.

- Monetization efficiency: Anthropic generates roughly $211 per monthly user versus OpenAI's approximately $25 per weekly user, an 8x difference.

- Enterprise concentration: 85% of Anthropic's revenue comes from business customers. 85% of OpenAI's comes from individual ChatGPT subscriptions.

Anthropic has hired Wilson Sonsini to prepare for a potential IPO. At $380 billion on $19 billion annualized revenue, it trades at approximately 20x ARR with a credible path to positive cash flow by 2027. PitchBook ranks OpenAI weakest on business quality fundamentals among the three major AI IPO candidates (OpenAI, Anthropic, Databricks) despite commanding the highest valuation.

The Wall Street Journal reported this week that OpenAI is reconsidering its strategy, potentially pivoting from consumer bets (video generators, browsers, devices) toward a tighter enterprise focus. If confirmed, this is a tacit acknowledgment that Anthropic's model is working.

Signal 3: State AI Governance Acceleration

- Tennessee: HB 1455 creates a Class A felony for training AI to encourage suicide. Scheduled for Judiciary Committee hearing April 7.

- Utah: Governor Cox signed nine AI-related bills in March, including deepfake protections and school technology restrictions.

- Vermont: H 814 (neurological rights) and H 816 (AI in mental health services) both passed the House and moved to Senate committees.

- Multiple states: AI-in-healthcare regulation advancing in Tennessee, Ohio, and Connecticut.

No federal preemption framework exists. The governance layer is arriving jurisdiction by jurisdiction, creating a compliance landscape that will force AI companies to either build for the most restrictive standard or maintain state-by-state compliance infrastructure.

Signal 4: The IPO Sequencing Game

Both OpenAI and Anthropic are preparing to list, potentially as early as Q4 2026. The sequencing matters enormously:

The first company to file an S-1 will establish the valuation framework for pure-play AI companies in public markets. It will also absorb the initial wave of retail investor demand for AI exposure. The second filer will compete for incremental capital.

Anthropic's enterprise-first model, higher revenue per user, and closer proximity to profitability may prove more legible to public market investors than OpenAI's larger but loss-making consumer model. If Anthropic files first, OpenAI's IPO could face a more skeptical reception.

The reverse is also true: if OpenAI files first at $850B+ and the stock performs well, it could set a ceiling that makes Anthropic's $380B valuation look modest.

Signal 5: Liberation Day's Lingering Effects

One year after Liberation Day, the data tells a clear story:

- Manufacturing employment has declined by 89,000 jobs since April 2025

- The U.S. goods trade deficit was $901.5 billion in 2025, essentially unchanged from 2024

- China ended 2025 with a record $1.2 trillion trade surplus

- FDI into the U.S. totaled $288.4 billion in 2025, below the prior 10-year average

The tariff regime did not achieve its stated objectives of increasing manufacturing employment or reducing the trade deficit. It did succeed in raising the cost of AI infrastructure inputs and creating permanent uncertainty in chip supply chains. For AI investors and operators, the lesson is that trade policy has become a structural variable, not a cyclical one.

III. Correspondent Dispatches

Overall confidence level: MIXED (High on revenue data, Low on valuation frameworks)

The revenue numbers are the most reliable data in the current AI landscape. Both OpenAI and Anthropic calculate annualized revenue using comparable methodologies: trailing 4-week revenue multiplied by 13 for API revenue, plus monthly recurring subscription revenue multiplied by 12. These are not projections. They are math applied to real billing data.

What is unverified:

1. Margin sustainability. Anthropic has revised its gross margin projection downward to approximately 40%, ten percentage points below earlier expectations. The compression comes from inference costs on Google and Amazon infrastructure. As revenue scales, inference costs scale with it. The path from 40% gross margin to positive free cash flow depends on inference cost per token declining faster than usage grows. This is plausible but unproven at the current scale.

2. Valuation coherence. OpenAI at $852 billion on $25 billion ARR with $14 billion in projected losses trades at metrics that have no historical precedent in enterprise software. Anthropic at $380 billion on $19 billion ARR with a path to 2027 profitability is more legible but still requires sustained 3-4x annual growth.

3. Tariff impact quantification. CSIS estimates $75-100 billion in additional costs. This range is wide enough to encompass scenarios from modest (10% cost increase on specific chip imports) to severe (broad semiconductor tariffs after the July 1 report). Treat the estimate as directionally correct but not precise.

Leading indicator to watch: Anthropic's Q2 2026 revenue trajectory. If the annualized rate crosses $22-25 billion by June, the convergence with OpenAI is confirmed and the IPO timeline accelerates. If growth decelerates to the internally projected 4x annual rate, the crossover pushes to 2027.

Falsification criteria: If hyperscaler capex guidance for 2027 declines sequentially from 2026 during Q1 earnings calls (mid-April), the thesis that AI infrastructure spending is structurally higher breaks. This would be the most bearish signal in the current cycle.

Phase transition identified: The Valuation Layer

The system has entered a new phase. For the first time, public markets will be asked to price the AI transition directly. Every prior valuation, from Nvidia at $3 trillion to Microsoft's AI premium, has been a derivative bet: investors buying companies that benefit from AI without pricing the AI models themselves.

The IPO of either OpenAI or Anthropic will force a direct answer to the question: what is a foundation model company worth?

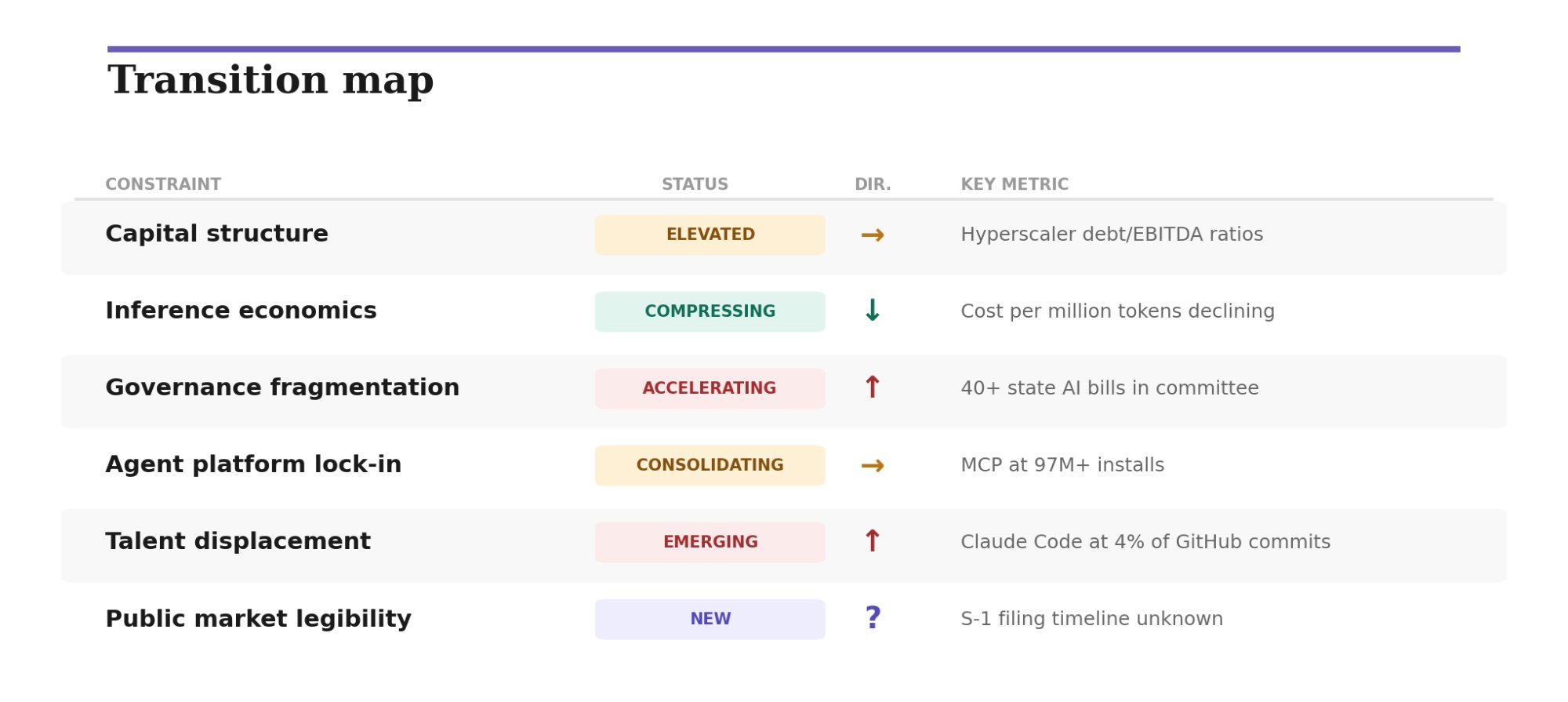

The binding constraints have shifted. In Issue 001, we identified five constraints: capital structure, inference economics, governance fragmentation, agent platform lock-in, and talent/labor displacement. This week, we add a sixth: public market legibility. The companies that can explain their unit economics in an S-1 that public market analysts understand will command valuation premiums. Those that cannot will face discounts.

The strategic landscape:

Anthropic holds a structural advantage in the IPO race:

- Enterprise revenue concentration (85% from businesses) matches the SaaS metrics public markets know how to value

- Revenue per user ($211/month) is 8x OpenAI's, suggesting pricing power

- Path to 2027 profitability provides a discounted cash flow anchor

OpenAI holds a narrative advantage:

- Largest brand recognition in AI

- Broader product surface (ChatGPT, DALL-E, Sora, enterprise platform)

- The Stargate infrastructure project with SoftBank signals nation-state-level ambition

The tariff-IPO coupling. Tariff uncertainty directly impacts the profitability timeline for both companies. Higher infrastructure costs compress gross margins, which makes the path to profitability longer, which makes the S-1 story harder to tell. This creates an incentive for both companies to file before the July 1 Commerce semiconductor report, which could introduce new tariff authority.

Action policy: Position for a Q3-Q4 2026 filing window. Anthropic files first in the base case. The filing will be the most important document in AI since the original GPT-3 paper, because it will contain the first audited unit economics for a pure-play AI lab.

One year after Liberation Day, the pattern is familiar. The American railroad buildout of the 1860s and 1870s was funded, like the AI buildout today, on leverage. Railroad companies issued bonds backed by the promise of future freight revenue that had not yet materialized. When Jay Cooke & Company, the most prominent railroad financier, failed in September 1873, it triggered the Panic of 1873 and a depression that lasted six years.

The parallel is not exact. Hyperscalers have balance sheets that Jay Cooke could not have imagined. But the structural dynamic is identical: massive capital deployed in advance of proven monetization, funded increasingly by debt, with the assumption that demand will materialize to justify the expenditure.

The question Darśan would ask is not whether demand will materialize. It almost certainly will. The question is whether it will materialize fast enough, at sufficient margin, to service the leverage that funded the buildout. This is the fulcrum.

The tariff episode adds a dimension the railroads did not face: input cost volatility imposed by sovereign policy. The railroads could at least forecast the cost of steel and labor. AI infrastructure builders cannot forecast the cost of their most critical input (advanced chips) more than six months ahead, because that cost depends on trade policy decisions made by a single executive branch.

First principles: In transitions, the greatest risk is not that the new thing fails. It is that the financing structure of the new thing is mismatched to the timeline of its success. The AI transition will succeed. The question is whether the current financing structure, $700 billion in capex funded by $400 billion in new debt and $852 billion private valuations, is the structure that survives to see that success.

Build for resilience. The companies that survive the financing correction, when it comes, will be the ones that own their unit economics and can demonstrate profitability on a per-customer basis. The S-1 filings will reveal who can do this and who cannot.

IV. Transition Map Update

| Constraint | Status | Dir. | Key Metric |

|---|---|---|---|

| Capital structure | Elevated | → | Hyperscaler debt/EBITDA ratios |

| Inference economics | Compressing | ↓ | Cost per million tokens (declining) |

| Governance fragmentation | Accelerating | ↑ | State AI bills in committee (40+) |

| Agent platform lock-in | Consolidating | → | MCP installs (97M+) |

| Talent/labor displacement | Emerging | ↑ | Claude Code GitHub commit share (4%) |

| Public market legibility | NEW | ? | S-1 filing timeline |

V. Scenario Analysis

Base Case (55% probability): Ordered IPO Sequence

- Anthropic files S-1 in Q3 2026. IPO in Q4 2026 or Q1 2027. Prices at 20-25x forward revenue.

- OpenAI follows 3-6 months later. No new semiconductor tariffs before filings.

- Q1 earnings confirm capex guidance.

Upside Case (25% probability): AI Revenue Acceleration

- Both Anthropic and OpenAI exceed revenue projections by 30%+.

- Enterprise AI spending broadens beyond coding tools to sales, legal, and operations.

- IPO valuations exceed private market levels. Semiconductor tariffs deferred or exempted.

Downside Case (20% probability): Margin Compression Meets Tariff Escalation

- Commerce recommends broad semiconductor tariffs in July.

- Inference costs fail to decline at projected rates. IPO filings reveal margins worse than expected.

- One or both companies delay IPO to 2027. Public market sentiment toward AI sours.

VI. Audience-Specific Action Items

For Investors

- Monitor Anthropic's revenue trajectory through Q2 for convergence confirmation.

- Track the Commerce semiconductor report (due July 1) for tariff risk repricing.

- Prepare frameworks for valuing pure-play AI companies ahead of S-1 filings.

- Consider exposure to AI infrastructure suppliers (indium phosphide, optical transceivers) where tariff dynamics create mispriced assets.

For Operators

- Audit AI infrastructure contracts for tariff exposure on chip imports.

- Accelerate evaluation of inference-optimized silicon alternatives (Cerebras, Trainium, TPU).

- Build compliance playbooks for state-level AI regulation (Tennessee, Utah, Vermont as templates).

- Evaluate Claude Code and competing AI coding tools for developer productivity ROI.

For Policymakers

- The Commerce semiconductor report due July 1 will set tariff expectations for the second half of 2026.

- State AI legislation is creating a patchwork that will eventually force federal action.

- IPO filings will create the first public disclosure of AI lab unit economics, informing regulatory impact assessments.

For Board Members

- Request briefings on enterprise AI vendor concentration risk (Anthropic vs. OpenAI).

- Assess board readiness for AI governance compliance across multiple state jurisdictions.

- Evaluate whether current AI infrastructure procurement contracts include tariff escalation clauses.

- Consider the strategic implications of AI lab IPOs on your company's competitive positioning.

In the Anthropocene, certainty was a luxury you could purchase.

In the Novacene, resilience is the only certainty that compounds.

If it's real, it will survive instrumentation.